Who Is Required to Pay the PCORI Fee? A Simple Guide

If there is one compliance question benefits teams ask every spring, it is this one, who is required to pay the PCORI fee? The answer depends on how your health coverage is funded, and whether certain arrangements count as “applicable self-insured health plans” under the law. This guide makes the decision simple, with a quick decision map, a comparison table, current market context, and practical filing tips.

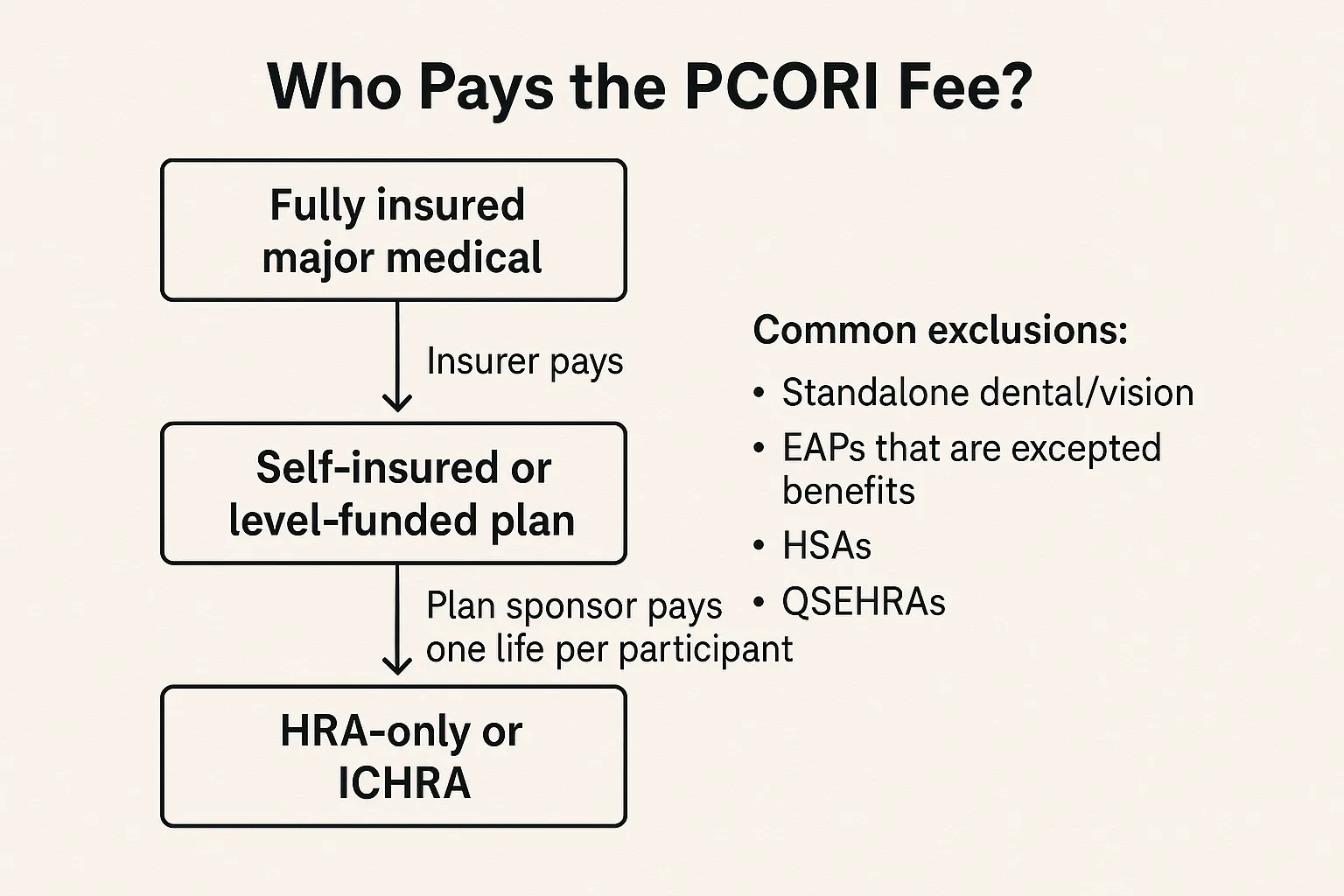

The 30-second answer

The Patient-Centered Outcomes Research Institute fee helps fund comparative clinical effectiveness research. It is reported and paid annually on IRS Form 720 and is due by July 31 for plan years that ended in the prior calendar year. In general:

If your major medical coverage is fully insured, the insurer pays the PCORI fee for that policy. You may still owe a separate fee if you sponsor an HRA.

-

If your major medical coverage is self-insured or level-funded, the plan sponsor, typically the employer, pays the PCORI fee.

Who pays, and who does not, at a glance

| Arrangement | Who pays the PCORI fee | What to know |

|---|---|---|

| Fully insured group health plan | The insurer | Employer generally has no PCORI liability for the insured policy, but see HRA row. |

| Self-insured or level-funded major medical | The plan sponsor | Most mid-size and large employers that self-fund must file and pay via Form 720. |

| HRA integrated with insured major medical | The employer, for the HRA only | Count one life per HRA participant, dependents are not counted. The insurer pays PCORI for the insured medical plan. |

| HRA integrated with self-insured major medical | The plan is treated as a single self-insured plan | Pay PCORI form 720 once on the combined plan, no separate HRA fee. |

| ICHRA (individual coverage HRA) | The employer | Treated as a self-insured arrangement for PCORI purposes, generally one life per participant. |

| COBRA or retiree-only self-insured coverage | The employer | PCORI applies to these covered lives. |

| QSEHRA | Generally not subject | QSEHRAs are not group health plans under the Code, which removes PCORI exposure. See IRS guidance. |

| Excepted benefits, for example standalone dental or vision, certain EAPs, onsite clinics, and most health FSAs that are excepted benefits | Not subject | Excepted benefits are outside the PCORI fee. HSAs and Archer MSAs are also not subject. |

This table is a summary, always confirm how your specific plan is structured and whether it is an excepted benefit under 26 U.S.C. 9832 and related regulations.

Why this matters in 2026

The share of covered workers enrolled in self-funded health plans remains high. The KFF 2024 Employer Health Benefits Survey reports that about 65 percent of covered workers are in self-funded plans, a level that has stayed elevated for several years. That means a large share of employers, especially those with 200 or more employees, are directly responsible for the PCORI fee each July and must report it through Form 720 excise tax filings. As more small and mid-size employers adopt level-funded or self-funded designs and HRAs, it is increasingly important to identify who owes the fee inside your organization and to standardize your data collection process early each year.

Counting covered lives correctly

Your PCORI fee equals the IRS-published dollar amount multiplied by average covered lives. For self-insured plans, you can use one of the IRS-approved methods. The method you choose must be applied consistently for the entire plan year.

Actual count method, average the total lives covered on each day of the plan year.

-

Snapshot method, use specified dates in each quarter and average the counts. A related snapshot factor method allows a simplified factor for non self-only tiers.

-

Form 5500 method, derive the average from the participant counts reported on the Form 5500, subject to timing rules.

Special rule for HRAs and some account-based plans, when an HRA is subject to form 720 PCORI and is not combined with a self-insured medical plan, you may count one life per participant. Dependents and other beneficiaries are not counted for the HRA.

Filing deadlines, amounts, and where to report

Due date, July 31 following the end of the plan year. A calendar-year plan ending December 31, 2025 is due July 31, 2026.

-

Form, report and pay on the second-quarter Form 720, Quarterly Federal Excise Tax Return, in Part II where the PCORI line appears. If you do not have other excise tax liabilities, you file only for the second quarter to report the PCORI fee.

-

Dollar amount, the per-life fee is indexed annually. For example, the amount for plan years ending in 2023 was 3.00 dollars per covered life, and for plan years ending on or after October 1, 2023 and before October 1, 2024 it increased to 3.22 dollars per covered life. The IRS issues a notice each year with the applicable amount. Always confirm the latest rate for your plan year.

Real-world scenarios and lessons learned

A 150-employee manufacturer with an insured medical plan and a traditional HRA, the insurer pays PCORI on the policy. The employer still owes PCORI for the HRA, but can count one life per HRA participant. Lesson, do not overlook HRAs, they often create a separate PCORI filing.

-

A 900-employee tech firm with a self-insured PPO and an integrated HRA, treat the PPO and HRA as one self-insured plan. Pay PCORI once, use the same counting method, and avoid double counting. Lesson, map your plan aggregation rules before you calculate covered lives.

-

A nonprofit with a retiree-only self-insured medical plan, PCORI still applies. Lesson, retiree-only does not exempt a self-insured plan from PCORI.

-

An association MEWA with multiple participating employers, the plan sponsor, commonly the board of trustees, files and pays. Lesson, confirm who the legal plan sponsor is, then coordinate data intake across participating employers to avoid missed lives.

Strategy checklist for clean PCORI compliance

Lock your funding status early, document whether each medical arrangement is insured or self-insured and whether any component is an excepted benefit.

-

Choose your counting method in Q1, and confirm that payroll, TPA, and enrollment vendors can deliver the counts in the format and timing you need.

-

Use the Form 5500 method only if your filing timeline supports it. If your 5500 is not final by July, use snapshot or actual count instead.

-

For HRAs, keep a separate participant roster. The one-life rule is a compliance advantage, but only if your data is clean.

-

Archive your workpapers. IRS examinations typically focus on method consistency, documentation, and whether you included all applicable arrangements.

How to file the PCORI 720 form online in minutes

With the deadline falling during busy mid-year close, e-filing can save time and reduce avoidable errors.

Create a free account at eFileExcise720, https://www.efileexcise720.com

-

Start a new Form 720, pick the second quarter, and complete the PCORI section in Part II. Enter your average covered lives and the IRS-published per-life amount for your plan year end.

-

Add payment details, you can pay electronically using EFTPS or other IRS-accepted methods.

-

Review and transmit, get an IRS acknowledgment, then save your proof of filing for your audit file.

E File Excise 720 is an IRS-authorized e-filing provider, designed for fast, secure Form 720 online filing. If you’re wondering what if Form 720 needs correction or late filing, the platform supports all Form 720 categories, including 720-X for amendments when you need to correct a prior PCORI filing, and offers personalized support that understands employer health plan nuances. No software download is required.

Key takeaways you can act on this quarter

Identify whether each of your health benefits is insured or self-insured, and whether any arrangement is an excepted benefit. This alone determines who pays in most cases.

-

If you sponsor an HRA or ICHRA, you likely owe PCORI. Use the one-life per participant rule where permitted.

-

Calendar your July 31 deadline and collect counts by late May. Adopt one IRS-approved counting method and stick with it across the plan year.

-

File IRS online to reduce risk. Using eFileExcise720 for efile Form 720 keeps your audit trail tidy and your submission on time.

Our services are also available for 720 filing California, 720 filing Florida, Form 720 filing New Jersey, Form 720 filing Ohio, Form 720 Filing Georgia, Form 720 filing Pennsylvania, 720 filing Illinois, and form 720 filing Texas.