What Is Domestic Petroleum Oil Spill Tax? A Complete Guide

The Domestic Petroleum Oil Spill Tax is one of those excise taxes that many businesses only notice when a quarter-end close reveals a mismatch between operational volumes and what the IRS expects on Form 720. If you refine crude oil, import taxable petroleum products, or manage fuel tax compliance for a growing energy or logistics business, understanding this tax is less about definitions and more about building a repeatable process that survives audits, acquisitions, and shifting supply chains.

This guide explains what the Domestic Petroleum Oil Spill Tax is, who pays it, how it’s calculated and reported on Form 720, and where Form 8849 can come into play for claims.

What is the Domestic Petroleum Oil Spill Tax?

The Domestic Petroleum Oil Spill Tax is a federal excise tax tied to the Oil Spill Liability Trust Fund (OSLTF), a fund designed to support oil spill response and certain cleanup costs when responsible parties cannot or do not pay.

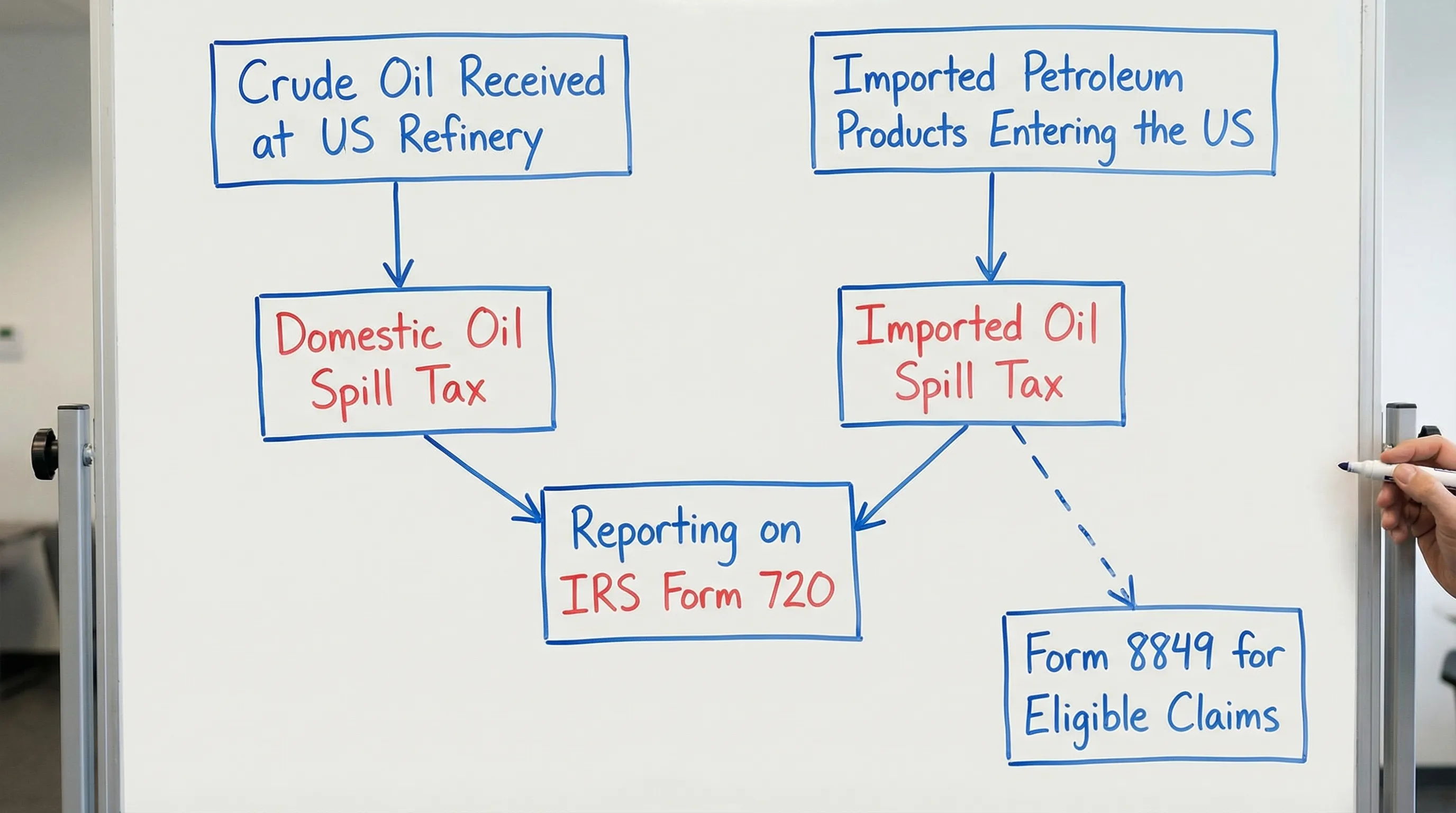

In practice, the tax is imposed per barrel on:

- Domestic crude oil received at a U.S. refinery (often referred to as the domestic oil spill tax), and

- Taxable petroleum products entering the U.S. for consumption, use, or warehousing (commonly discussed as the Imported Petroleum Products Oil Spill Tax).

Although people use slightly different labels in conversation, both pieces are commonly reported through the excise tax system on Form 720.

Who owes the tax? Domestic vs. imported triggers

For compliance teams, the most important step is identifying the taxable event and the liable party.

Domestic petroleum crude oil received at a refinery

The tax generally applies when crude oil is received at a U.S. refinery. Typically, the refinery operator is the party with the reporting obligation, because the taxable moment is tied to receipt at the refinery.

Operationally, this means your tax numbers tend to come from measurement systems and custody transfer records, not from your general ledger alone. Many errors happen when companies rely on financial volume summaries that were never designed to align with tax definitions.

Imported petroleum products (entry into the U.S.)

The Imported Petroleum Products Oil Spill Tax generally applies when taxable petroleum products enter the United States for consumption, use, or warehousing.

This is where trade documentation matters. Your importer-of-record data, customs entries, and product classifications often become the “source of truth” for excise tax reporting. If your supply chain includes marine shipments, transshipment points, or storage in multiple jurisdictions, legal and documentation rigor becomes a competitive advantage. For cross-border shipping and spill-liability considerations, some businesses also consult admiralty and shipping counsel to pressure-test contracts, risk allocation, and incident-response obligations.

How much is the Oil Spill tax?

The tax is assessed per barrel, and the applicable rate can change by statute, so treat the IRS instructions as your final source for the current quarter.

A practical way to make this actionable for forecasting is to model the tax as a direct “per-barrel” compliance cost alongside logistics, RINs (if applicable), and storage. Even small rate changes become material at scale.

The table below shows illustrative tax cost at a $0.10 per barrel rate (use this as a planning example and confirm the rate in the current Form 720 instructions before filing).

| Barrels in the Quarter | Example Rate (Per Barrel) | Illustrative Tax Cost |

|---|---|---|

| 50,000 | $0.10 | $5,000 |

| 250,000 | $0.10 | $25,000 |

| 1,000,000 | $0.10 | $100,000 |

| 5,000,000 | $0.10 | $500,000 |

Why this matters strategically: in acquisition diligence (or even lender reporting), buyers and investors often focus on environmental exposure and tax compliance posture. A per-barrel excise that looks small can become a six-figure quarterly liability, plus penalties and interest, if the process breaks during a system migration.

How to report the Domestic Petroleum Oil Spill Tax on Form 720

The Oil Spill tax is reported on IRS Form 720 (Quarterly Federal Excise Tax Return). Most filers think of Form 720 as “one tax return,” but in reality it is a container for many excise categories. That’s why reconciliation discipline matters: the same quarter may require environmental items, fuel-related items, and even benefit-plan related fees.

Filing cadence and operational timing

Form 720 is filed quarterly, with due dates that are fixed to the calendar:

| Quarter | Typical Period Covered | Form 720 Due Date |

|---|---|---|

| Q1 | Jan – Mar | April 30 |

| Q2 | Apr – Jun | July 31 |

| Q3 | Jul – Sep | October 31 |

| Q4 | Oct – Dec | January 31 |

If a due date falls on a weekend or legal holiday, it generally shifts to the next business day (confirm for the year you are filing).

The data you want ready before you file

To reduce quarter-end surprises, build a single package that ties directly to taxable events:

- Barrel volumes by taxable event (domestic refinery receipt vs. imported product entry)

- Product and transaction support (tickets, bills of lading, custody transfer documents)

- Import documentation (where applicable)

- Prior-quarter adjustments (returns, reclassifications, late operational corrections)

If you need technical interpretation help, the IRS instructions for Form 720 are the best starting point, and IRS customer support can help with certain procedural questions. But the IRS will not reconcile your internal measurement systems for you, that work has to be done in-house or with a qualified advisor.

When Form 8849 matters (and when it doesn’t)

In the Form 720 world, two forms get confused all the time:

- Form 720 is where you report quarterly excise tax liability.

- Form 8849 is commonly used to claim certain refunds or credits when you qualify under specific rules.

For the Oil Spill tax, Form 8849 may come into play in scenarios where the rules allow a claim (for example, certain eligible uses, re-exports, or other claim situations depending on the category and facts). The key is documentation. Claims without tight support are the first thing to get delayed.

If you discover an error on a previously filed quarter, the fix may involve an amendment (often via Form 720-X, depending on the correction type) rather than trying to “wash it out” in a future quarter.

Comparisons: why this tax behaves differently than other Form 720 items

Oil Spill tax compliance sits at the intersection of operations and tax, which is not always true for other Form 720 categories.

| Form 720 Item | What Drives the Numbers | Common Failure Point |

|---|---|---|

| Domestic Petroleum Oil Spill Tax | Physical volumes and taxable events | Measurement, timing cutoffs, refinery receipt definition |

| Imported Petroleum Products Oil Spill Tax | Customs entry and classification | Data handoffs between trade compliance and tax |

| Ozone-Depleting Chemicals Excise Tax | Chemical/product taxonomy and importer/producer facts | Misclassification, missing product detail |

| PCORI Fee | Covered lives and plan structure | Counting method errors, missed July filing |

This comparison is useful because it informs staffing. If your Oil Spill tax reporting is owned solely by accounting, but the source data lives in terminals, refinery systems, or customs brokers, you have a structural risk.

2026 trends and strategic advice for staying audit-ready

Three patterns are showing up more often as excise teams modernize:

First, companies are moving from “quarterly scramble” to continuous reconciliation. The goal is to catch volume anomalies in week two, not week twelve.

Second, more businesses are building controls that survive M&A. A common lesson learned is that acquired entities may track barrels differently. If you do not normalize definitions immediately, your first combined Form 720 can be wrong even if both legacy filings were “right” on their own.

Third, more executives want compliance clarity on cost. Treat Oil Spill tax like a measurable unit cost. When you can forecast it per terminal, per product stream, or per supply lane, you can spot anomalies early and explain changes to leadership without guesswork.

Filing efficiently (without turning this into a bigger project than it needs to be)

If you prefer to file electronically, E File Excise 720 (eFileExcise720) is an IRS-authorized platform designed to help businesses e-file Form 720 online, including support for all Form 720 categories, amendments (720-X), and Form 8849 claims, with secure data handling and personalized customer support.

If you’re evaluating vendors, compare pricing based on how many categories you file and whether you anticipate amendments or claims. If you want help mapping your oil spill tax data to the right Form 720 sections, you can also contact us through the site to discuss your filing needs.