Does Your Business Need to File Form 720 What You Should Know

Starting a new venture or managing an established company already involves enough compliance paperwork. Yet the IRS still expects certain businesses to submit Form 720, the Quarterly Federal Excise Tax Return, whenever they sell or use specific goods and services. Confusion about who must file creates three common scenarios:

-

Owners who should file but do not realize it until they receive a penalty notice.

-

Businesses that file when they are not actually liable, wasting both time and money.

-

Teams that file late because they underestimated the data required for each taxable activity.

If you have ever wondered whether Form 720 applies to your organization, this guide walks through the must-know facts: who is required to file, which products and services trigger filing, key deadlines and smart tips for staying compliant with minimal effort.

1. What Form 720 Covers in Plain English

Form 720 is the IRS’s mechanism for collecting federal excise taxes on a wide range of activities, from aviation fuel sales to indoor tanning services. While income tax focuses on profits, excise tax targets specific goods, services, or usages and is often embedded in the price paid by the ultimate consumer. To ensure accurate reporting and compliance, businesses should carefully review and follow the official form 720 filing instructions when preparing and submitting their returns.

Most of the 50+ excise taxes currently collected fall into one of four buckets:

| Bucket | Typical Industries Affected | Examples of Taxable Activities |

|---|---|---|

| Environmental Tax | Chemical manufacturers, importers, oil refineries | Ozone-depleting chemicals, petroleum superfund tax |

| Communications & Air Transport | Airlines, air cargo operators, telecom providers | Passenger ticket tax, air cargo tax, cable TV and satellite tax |

| Fuel | Trucking fleets, fuel wholesalers and retailers, railroads | Diesel, gasoline, kerosene, alternative fuels |

| Manufacturers & Retail Services | Medical plans, firearm makers, tanning salons | PCORI fee, firearms tax, indoor tanning tax |

Because the list is updated by Congress from time to time, always review the latest IRS Instructions for Form 720 (Rev. June 2024) before deciding whether you owe tax.

2. The Straightforward Filing Test

Determining your obligation boils down to a two-step test:

-

Did your business sell, manufacture, import, or use any products or services listed in Parts I or II of Form 720 during the quarter?

-

If so, do the tax rate and the exemption limit actually leave you with any tax to pay for that period, or does it still come out to zero?

You must answer “yes” to both questions to trigger a filing requirement. For example, a small charter airline that flew taxable passenger segments owes excise tax even if it operated at a loss for income-tax purposes. Conversely, a tanning studio that was closed all quarter would not file because it had no indoor tanning revenue to report.

3. Common Business Profiles That Must File

While every situation is unique, the IRS’s own audit data suggests nine categories account for the majority of IRS tax form 720 submissions:

Health insurers and self-insured employers paying the Patient-Centered Outcomes Research Institute (PCORI) fee.

-

Fuel wholesalers and terminal operators that blend or import taxable fuel.

-

Trucking fleets that store dyed diesel for non-highway use but sell or use it in taxable operations.

-

Airlines and air charter brokers collecting federal air transportation excise taxes.

-

Chemical manufacturers and importers of taxable substances such as butane, benzene, or ammonia.

-

Indoor tanning salons charging customers for UV light services.

-

Firearms and ammunition manufacturers responsible for excise on sales.

-

Phone, internet and satellite providers that still remit federal communications excise taxes in specific cases.

-

Large voc tech schools and universities running in-house aviation programs subject to fuel excise.

If your organization fits one of these profiles, consider tax form 720 part of your quarterly compliance calendar.

4. Understanding the PCORI Fee: A Special Case

Since many employers only touch Form 720 when paying the 720 PCORI form fee, it is worth highlighting the special rules:

Who owes it?

Fully insured group health plans pay via their carrier, but self-insured employers (including HRAs and some FSAs) must file themselves.-

When is it due?

July 31 of the year following the plan year end. For calendar-year plans ending December 31 2024, the PCORI filing arrives July 31 2025. -

How is it calculated?

Covered lives × annual dollar rate ($3.22 for plans ending in 2024, per IRS Notice 2024-31).

Because the PCORI fee is reported on the second quarter Form 720 even if no other excise liabilities exist, many companies forget this one-time summer filing. Mark the date early to avoid the standard 5 percent per month late-filing penalty.

5. Key Deadlines and Periods You Cannot Miss

Form 720 follows the IRS’s quarterly cadence:

| Quarter | Activity Period | Due Date |

|---|---|---|

| Q1 | Jan 1 – Mar 31 | April 30 |

| Q2 | Apr 1 – Jun 30 | July 31 |

| Q3 | Jul 1 – Sep 30 | October 31 |

| Q4 | Oct 1 – Dec 31 | January 31 (following year) |

If the deadline falls on a weekend or federal holiday, it shifts to the next business day. Electronic payments of the underlying tax typically use the Electronic Federal Tax Payment System (EFTPS) and are due on the same date.

6. Penalties: What Happens When You Ignore Form 720

| Type | Amount | Trigger |

|---|---|---|

| Late filing | 5 percent of the tax due per month, up to 25 percent | Return not filed by deadline |

| Late payment | 0.5 percent of unpaid tax per month, up to 25 percent | Tax not fully paid by deadline |

| Accuracy-related | 20 percent of underpaid tax | Negligence or substantial understatement |

Seeking reasonable-cause relief is possible but requires detailed written support, such as records of natural disasters or serious illness affecting responsible employees. In most cases, proactive e-filing and prompt payment eliminate these risks entirely.

7. Why the IRS Encourages E-Filing (and So Should You)

Excise tax reporting isn’t what it used to be. The IRS updated the whole system a while back, and ever since then, more and more businesses have been switching over as they realize how much easier life gets with IRS-authorized providers like eFileExcise720.

Speed: Electronic submissions reach IRS systems instantly and accepted receipts usually arrive within minutes.

-

Accuracy checks: Built-in business rules flag missing schedules, mismatched EINs and mis-keyed dollar amounts before the return is transmitted.

-

Audit trail: Downloadable copies of Form 720, payment confirmations and amendment history live in one secure dashboard.

-

Amendments simplified: When corrections are needed, Form 720-X can be created from the original file, saving hours of data re-entry.

The IRS now requires electronic filing for certain high-volume filers under the e-file mandate finalized in TD 9972 (Feb 2024). Even if your business is exempt, electronic filing all but eliminates clerical-error notices and the postal lag that can jeopardize on-time compliance.

8. Quick Self-Assessment Checklist

Answer the questions below for each quarter. A single “yes” means you likely need to file Form 720 or its amendment:

Did we sell, manufacture, or import a taxable product listed in Part I or II?

-

Did we provide a taxable service (air transport, indoor tanning, telecom) this quarter?

-

Are we a self-insured health plan sponsor whose plan year ended during this quarter (for Q2 PCORI only)?

-

Did we use taxable fuel outside an exempt context or repurpose dyed fuel for highway use?

-

Did we file Form 720 last quarter? If the activity continues, we must file again.

Still uncertain? Review the current IRS Instructions and consult a tax professional. When it is time to transmit, an e-file solution like eFileExcise720 guides you through category-specific questions and prevents missed schedules.

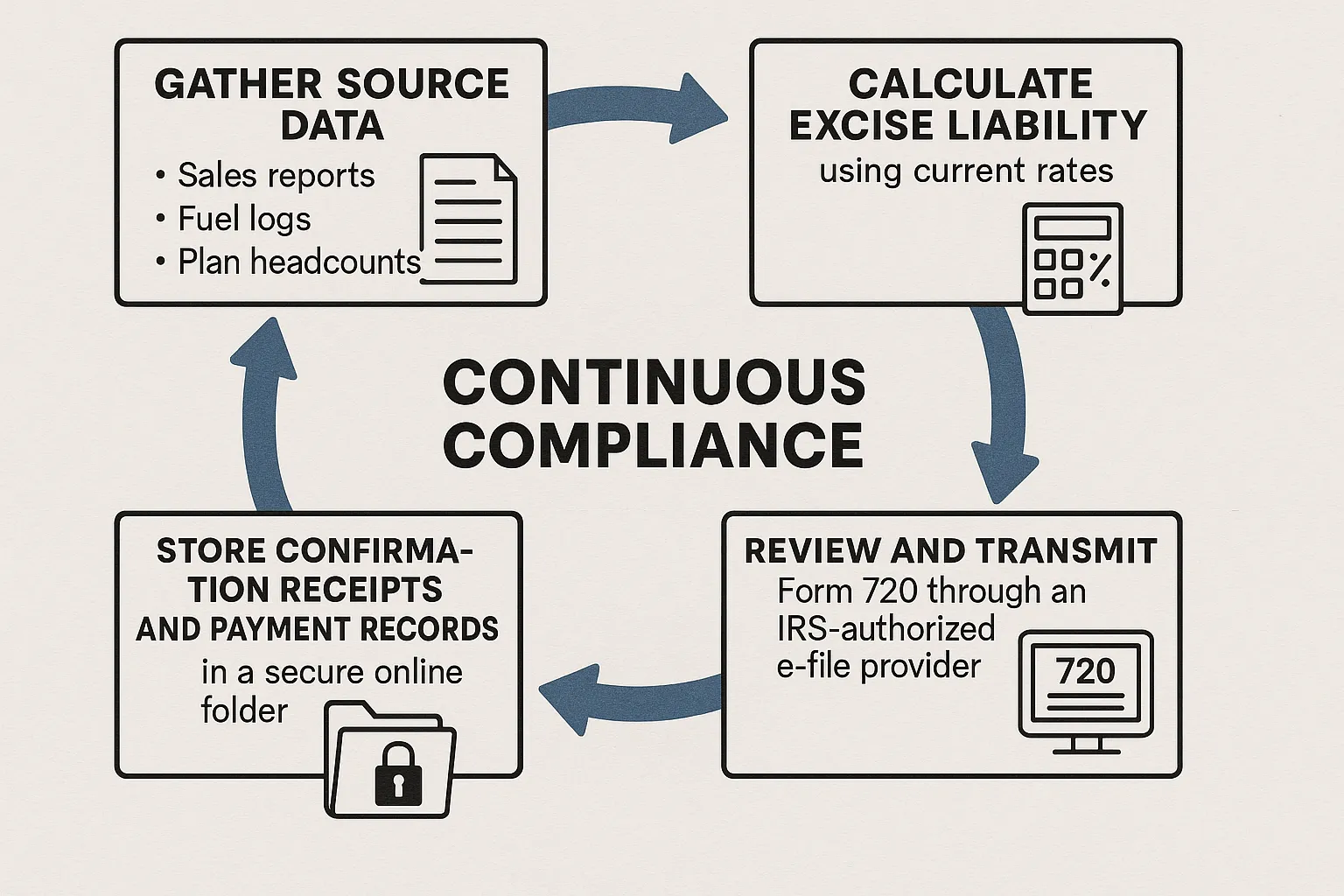

9. Filing Workflow in Four Steps

-

Gather source data: sales invoices, fuel withdrawals, PCORI head counts, or passenger segment logs for the quarter.

-

Calculate tax: apply current IRS rates, adjusting for exemptions or credits such as biodiesel mixtures.

-

Prepare and e-file: enter figures into each applicable Form 720 schedule, validate and transmit through eFileExcise720.

-

Archive and repeat: save the accepted return, EFTPS payment receipt and any exception reports to simplify future filings.

10. When Amendments Are Necessary

Mistakes happen. If you discover an overpayment or underpayment after filing, submit Form 720-X for that prior quarter. Common triggers include:

Receiving updated passenger counts from a code-share partner.

-

Reversing a fuel sale classified incorrectly as nontaxable.

-

Adjusting PCORI head counts following an eligibility audit.

eFileExcise720 lets you clone the original Form 720, make the delta adjustments and transmit the amendment in minutes, keeping your compliance trail intact.

11. Resources for Deeper Guidance

IRS Instructions for Form 720 (Rev. June 2024) – official reference for tax rates, exemptions and filing mechanics.

-

IRS Notice 2024-31 – annual PCORI fee rates and counting methods.

-

TD 9972 – e-file mandate regulations for excise tax forms.

-

https://www.efileexcise720.com/resources – step-by-step videos and industry-specific checklists.

The Bottom Line

If your business has anything to do with taxable fuels, certain chemicals, transportation stuff, tanning services, firearms, telecom, foreign insurance tax or even self-insured health plans, then Form 720 online filing isn’t something you can just skip. If you’re asking, “What is Form 720?”, it’s the IRS return used to report and pay these specific federal excise taxes. The good news is you don’t have to wrestle with those old paper instructions or wait around for the mailroom anymore just to stay compliant. With 2025 deadlines approaching, create your free account at eFileExcise720 today, follow the guided interview and file with confidence before the IRS ever sends a penalty notice.

Our services are also available for 720 filing California, 720 filing Florida, Form 720 filing New Jersey, Form 720 filing Ohio, Form 720 Filing Georgia, Form 720 filing Pennsylvania, 720 filing Illinois, and form 720 filing Texas.