What Is Manufacturing Tax? A Complete Guide for Businesses

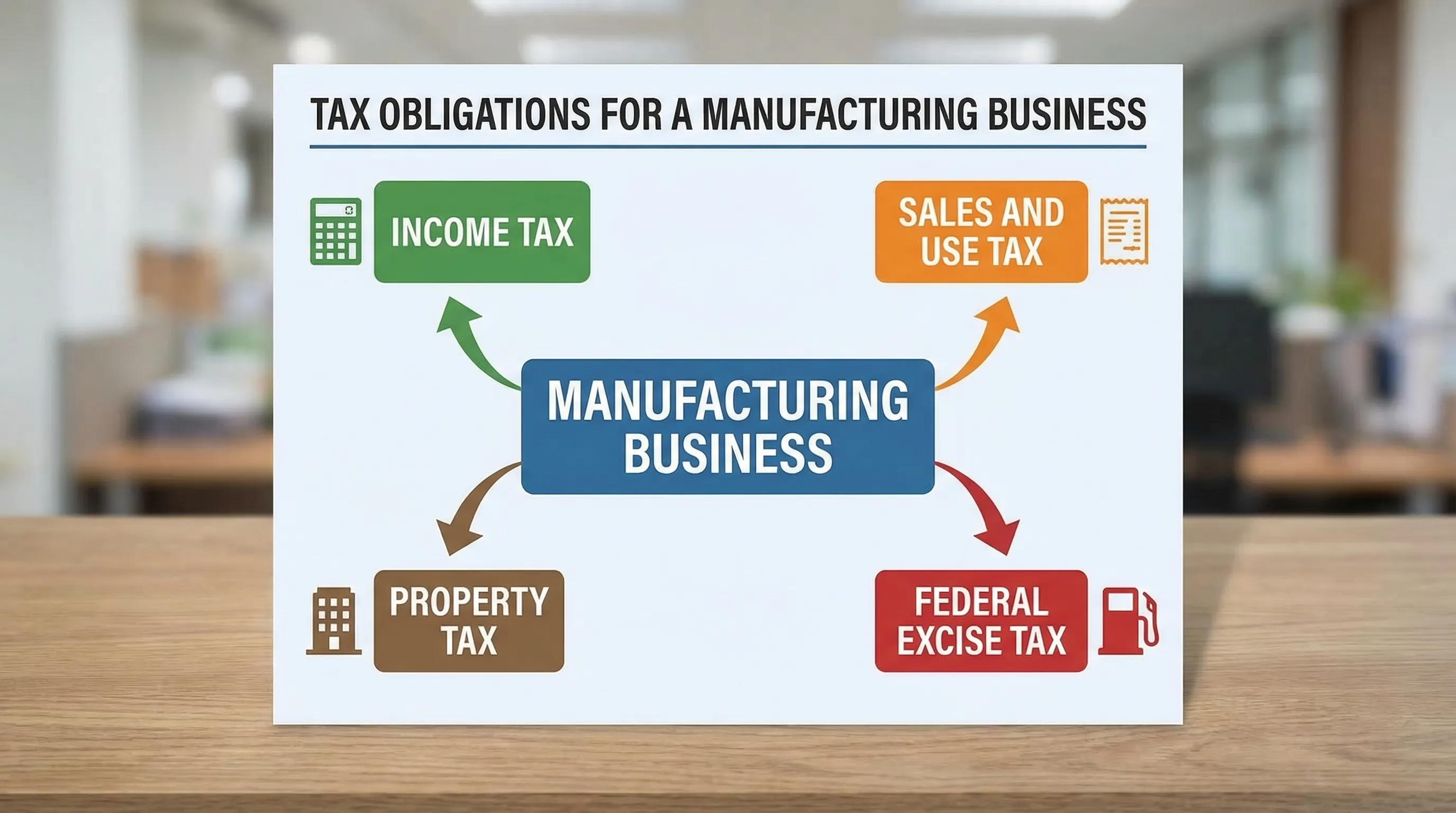

Most business owners hear manufacturing tax and assume it is a single, special tax for factories. In reality, manufacturing tax is a catch-all phrase that can refer to several different taxes that hit manufacturers at different points in the value chain, including income tax, sales and use tax, property tax, and often the most overlooked federal excise taxes reported on IRS Form 720.

This guide breaks down what is manufacturing tax, how to spot where your business is exposed, and how to build a compliance process that investors, lenders, and auditors tend to view as low risk.”

What is manufacturing tax

Manufacturing tax usually refers to the total tax burden associated with making and selling goods, not a single line item. It can include:

Taxes on profit (federal and state income taxes)

Taxes on purchases and transfers (sales and use taxes)

Taxes on assets (property tax on facilities and equipment)

Taxes on specific products or activities (excise taxes)

The gotcha is that excise taxes can apply even when profit is low, because they are often transaction-based (per unit, per gallon, or a percentage of sales price).

The manufacturing tax mix and why excise tax deserves special attention

Manufacturers often budget heavily for income tax planning, but excise taxes can create surprise liabilities because they hinge on product classification, the taxable event, and documentation.

Here is a fast comparison that helps teams align on what they are dealing with:

| Tax Type | What Triggers It | Typical Base | Why It Matters for Manufacturers |

|---|---|---|---|

| Income tax | Earning profit | Net income | Planning opportunities, but can be volatile with margins |

| Sales and use tax | Selling or buying taxable items | Transaction value | Nexus rules, exemptions, resale/manufacturing certificates |

| Property tax | Owning taxable property | Assessed value | Capex-heavy operations can see meaningful exposure |

| Federal excise tax | Making, selling, importing certain products, or performing taxable activities | Per-unit or % of price | Product-specific rules, deposits, audits, and refund claims |

From an investor perspective, excise tax risk is often treated like a hidden leverage factor because it can:

Reduce margins if pricing does not pass it through cleanly

Create working-capital strain if deposits are required

Trigger penalties if reported late or on the wrong tax code

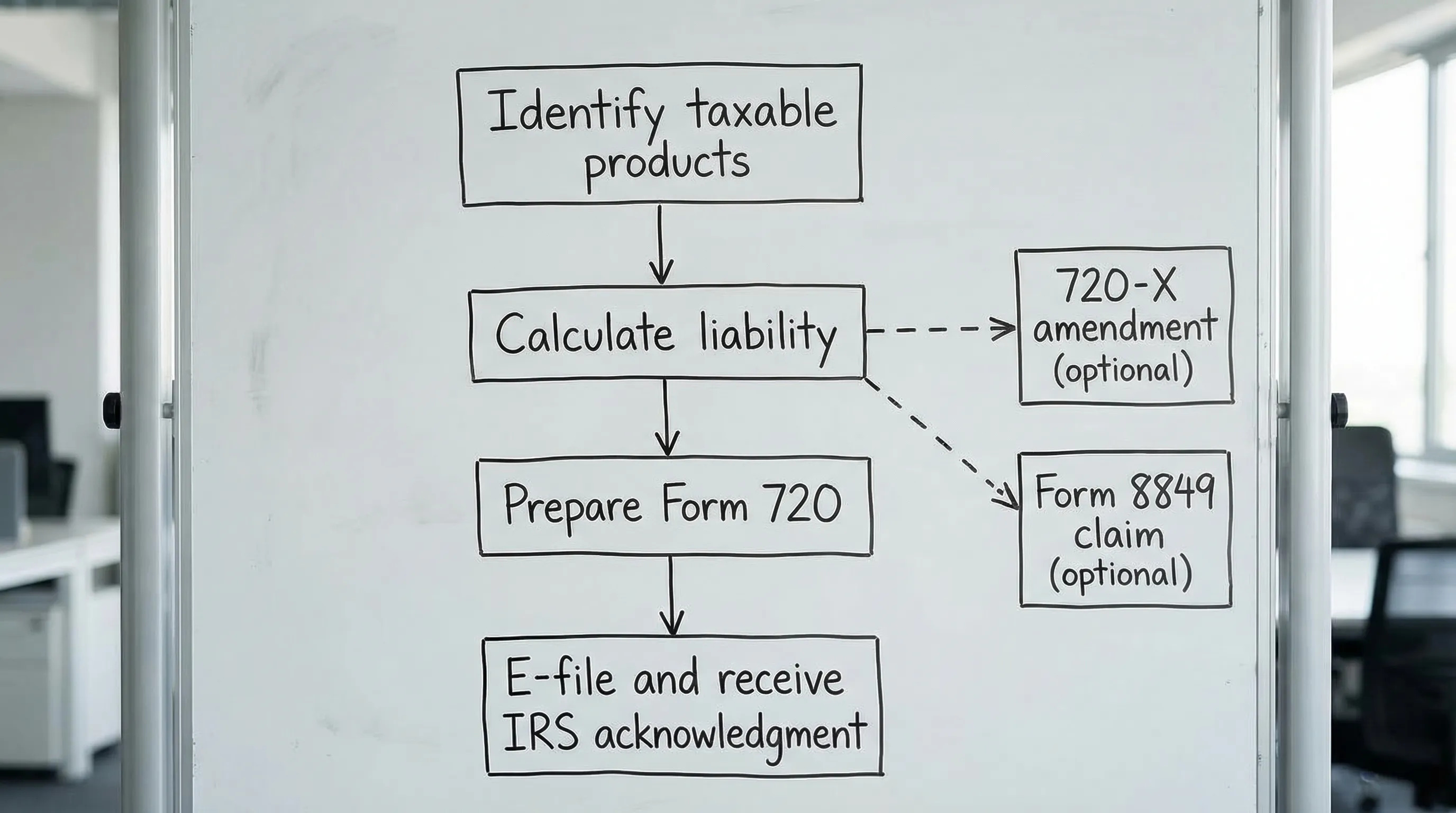

Manufacturing-related excise taxes and where Form 720 fits

Form 720 excise tax reporting is how many federal excise taxes are filed and paid. Form 720 is the quarterly federal excise tax return required by the IRS.

A key point: manufacturing excise taxes are not one uniform tax. They vary by product and activity. Examples of categories that can matter for manufacturing and industrial businesses include certain environmental and chemicals-related excise taxes, fuel-related taxes in specific scenarios, and other product-specific excise regimes depending on what you make or import.

To stay precise, always verify your applicable categories and tax codes in the official IRS materials for the current year, starting with the IRS Form 720 page and the form 720 filing instructions.

One of the most important recent shifts for industrial and chemical supply chains is the reinstatement of Superfund chemical excise taxes (effective July 1, 2022) under the Infrastructure Investment and Jobs Act. Many businesses discovered exposure not because they manufacture chemicals, but because they import or use taxable chemicals in a way that created reporting obligations.

The IRS maintains a hub for this topic, including guidance and lists, at its Superfund Chemical Excise Taxes resource.

Strategic advice: build a taxable product map like an investor would

When investors diligence manufacturing businesses, they rarely stop at Do you file taxes on time? They ask whether tax risk is systematized.

A strong approach is a taxable product map that ties together:

SKUs or product families

The taxable event (manufacture, sale, use, import, or other)

The applicable excise tax code (if any)

The evidence file (certificates, bills of lading, exemption support)

The reporting workflow (who prepares, who reviews, who files)

This matters because the most common real-world failure mode is not math, it is misclassification or missing documentation.

Form selection: Form 720 vs. tax form 8849 vs. 720-X

Manufacturing and distribution operations often need more than just the quarterly return.

| You need to… | Commonly Used Form | What It Does |

|---|---|---|

| Report and pay quarterly excise liabilities | Form 720 | Primary quarterly reporting vehicle |

| Correct a previously filed quarter | Form 720-X | Amendment workflow for prior periods |

| Claim eligible refunds/credits (when allowed) | 8849 form | Refund/claim form for specific excise tax situations |

If your situation calls for a claim, you may hear tax form 8849 described as the path to request a refund where permitted. As always, eligibility and substantiation are key, and you should align your claim approach with IRS instructions.

Where PCORI fits even if you are not a manufacturer

Many finance teams first encounter Form 720 through the PCORI Fee, which is reported annually on Form 720 even though Form 720 is otherwise quarterly.

Why mention PCORI in a manufacturing tax guide? Because it is a common example of how Form 720 obligations can appear outside “classic excise” industries. If your business sponsors certain self-insured health arrangements, the pcori 720 form workflow can become a recurring compliance item.

For a deeper PCORI-only walkthrough, see this related resource: Who is required to pay the PCORI fee?

Lessons learned from real investor due diligence

Public-company investors and private equity diligence teams tend to focus on a few repeatable questions:

- Is excise tax treated as pass-through or embedded cost? Some sectors disclose excise taxes that reduce net sales or affect revenue presentation. If pricing does not explicitly account for the tax, margin surprises follow.

- Is exposure tied to product mix changes? Launching a new product line, changing materials, or adding imports can create excise exposure even when the core business is unchanged.

- Is documentation audit-ready? The most expensive issues are often not the tax itself, but penalties, interest, and time-consuming exam support.

A practical move that sophisticated teams use is a quarterly tax close checklist parallel to the financial close, including review of product changes, shipping terms, and exemptions.

Actionable metric: why manufacturing tax planning is getting more board-level attention

Manufacturing remains a major part of the US economy roughly about a tenth of GDP in recent years, depending on the dataset and year. That scale draws regulatory attention, and it is one reason excise compliance is increasingly treated as a governance issue in larger companies.

You can explore industry GDP detail via the Bureau of Economic Analysis GDP by Industry data.

How to streamline form 720 online filing

If you file excise taxes, moving from manual workflows to form 720 online filing typically improves timeliness and reduces reject-risk because digital flows enforce required fields and support cleaner records.

eFileExcise720 is an IRS-authorized e-filing portal designed specifically for Form 720 and related excise filings. The platform supports Form 720 categories, amendments (Form 720-X), and claims support (Form 8849), with secure data handling and customer support.

If you want a separate operational checklist, this article is helpful alongside your close process: Form 720 e-filing checklist for 2026

Frequently Asked Questions

What is manufacturing tax?

Manufacturing tax is an informal term for the combined taxes that affect a manufacturer, including income tax, sales and use tax, property tax, and product or activity-based excise taxes.

Is there a specific federal manufacturing tax?

Not usually as a single tax. Most federal manufacturing-related obligations come through specific regimes like excise taxes on certain products or activities, which may be reported on Form 720 depending on the category.

What is Form 720 excise tax used for?

Form 720 is the IRS Quarterly Federal Excise Tax Return used to report and pay a range of federal excise taxes tied to specific products and activities.

What is the 8849 form used for?

The tax form 8849 (Form 8849) is used to claim refunds for certain excise taxes when the IRS allows a claim and you meet documentation requirements.

Is the PCORI Fee filed on Form 720?

Yes. The PCORI Fee is reported on Form 720 (often referred to as the pcori 720 form workflow) for applicable plan sponsors.

Can I amend an excise tax return after filing?

Yes, corrections are generally handled with Form 720-X, depending on the situation and IRS rules.

File Form 720 with an IRS-authorized e-file portal

If manufacturing tax in your business includes Form 720 excise tax, the easiest win is usually process improvement: clearer product mapping, cleaner documentation, and on-time e-filing.

To simplify filing, you can use efileexcise720.com to create a free account and e-file securely, without downloading software, with access to customer support when you need it.

Our services are also available for Form 720 filing California, Form 720 filing Florida, Form 720 filing New Jersey, Form 720 filing Ohio, Form 720 filing North Carolina, Form 720 filing Massachusetts, Form 720 filing Georgia, Form 720 filing Pennsylvania, Form 720 filing Illinois, and Form 720 filing Texas.