What Is Remittance Tax and Who Needs to Pay It?

“Remittance tax” is not a single tax with one rate. In the remittance tax USA context, it usually means a tax a business must send (remit) to a government agency after a taxable event happens, often after the business either collects the amount from customers (for example, certain transportation or communications charges) or incurs liability based on its operations (for example, certain fuel or environmental excise taxes).

For many U.S. organizations, the most common remittance-style taxes are federal excise taxes reported to the IRS on Form 720 (Quarterly Federal Excise Tax Return). If your company touches fuel, transportation, communications, manufacturing, or certain health-plan fees like PCORI, you may have a remittance obligation even if you do not think of yourself as a “tax business.”

What does “Remit” mean, and why it matters?

To remit means to pay over amounts owed to the IRS (or another taxing authority). The key compliance challenge is that the party who economically bears the tax (often the customer) is not always the party who is legally responsible for reporting and remitting it.

That gap drives most remittance-tax risk:

Pricing teams may bundle charges in ways that obscure taxable amounts.

Operations teams may trigger tax events (import, removal, sale, use) without a “tax” label.

Accounting teams may discover the obligation only after quarter-end.

If you are unsure whether a federal excise tax applies, start with IRS Form 720 and its official instructions, because many remittance-style federal excise obligations flow through this return. See the IRS pages for Form 720 and Instructions for Form 720.

Remittance tax USA: who usually needs to pay (remit) it?

You typically need to remit if you are the person liable under the excise tax rules for a transaction or activity that is covered by Form 720. That includes (but is not limited to) many organizations in these buckets:

Fuel supply chain: terminal operators, position holders, blenders, distributors, importers, and certain carriers, depending on the specific tax and taxable event.

Transportation and communications: airlines and service providers that bill taxable services (liability can sit with the provider, even if the customer “pays” the tax via the invoice).

Manufacturing and retail of certain products: businesses that sell or import specific goods subject to excise rules.

Employers and plan sponsors with self-insured health plans: entities responsible for PCORI filing (the PCORI fee is reported on Form 720).

Environmental and petroleum-related activities: certain taxes tied to chemical, petroleum, or environmental programs.

Quick comparison chart: “who pays” vs “who remits”

A practical way to explain remittance taxes to non-tax stakeholders is to separate economic incidence (who ultimately bears cost) from legal remittance responsibility (who must file and pay).

| Scenario (illustrative) | Who typically bears the cost? | Who typically must remit? | Common IRS form(s) involved |

|---|---|---|---|

| Taxable communications/transportation charge billed to a customer | Customer (via invoice) | Service provider / filer | Form 720 |

| Fuel-related excise triggered by removal, entry, or sale | Often passed through in price | Liable party in the chain (depends on facts) | Form 720; refunds may use Form 8849 |

| PCORI fee for a self-insured health plan | Employer/plan sponsor | Employer/plan sponsor | Form 720 (PCORI line) |

| Overpayment or eligible exempt fuel use | Business seeking recovery | Claimant | Form 8849 (often with schedules) |

How to tell if your business has a remittance tax obligation

Most businesses get into remittance tax trouble because they rely on “industry assumptions” (for example, “our vendor handles it” or “we pass it through, so it’s not ours”). A better test is operational:

1) Identify your taxable triggers

For federal excise taxes, triggers are event-based. Examples include:

Removing or selling certain fuels in a taxable manner

Importing certain products

Billing taxable services

Maintaining a self-insured plan requiring PCORI reporting

2) Map triggers to Form 720 lines and schedules

This is where Form 720 filing instructions matter. Form 720 is organized by categories, with specific line items and, in some cases, additional schedules.

If you have never done this mapping, the IRS instructions are the correct starting point (and are often what buyers, lenders, and auditors will reference when reviewing your process).

When remittance tax turns into refunds: Form 720 vs Form 8849 (and Schedule 1)

Remittance does not always mean “money only goes out.” Some excise tax situations create credits or refunds when the tax was overpaid or when fuel was used in an exempt way.

Form 720 is generally where you report and pay quarterly excise tax.

Form 8849 is generally where you claim a refund of certain excise taxes.

One common area is fuel. Form 8849 Schedule 1 (often searched as schedule 1 form 8849 or form 8849 schedule 1) is used for certain claims related to nontaxable uses of fuels (eligibility depends on facts and documentation). The IRS provides official references for Form 8849.

Strategic lesson: if your organization has both taxable and exempt use cases, you want a system that can support both clean remittance on Form 720 and defensible claims on Form 8849, with audit-ready records.

A due diligence lens: why investors scrutinize remittance tax

Remittance tax risk often shows up during mergers, acquisitions, and financing because it can behave like a “silent liability.” Here are real-world patterns investors and acquirers regularly flag (examples are representative scenarios, not specific companies):

Private equity-backed logistics roll-up: an acquired fleet had inconsistent fuel documentation. Post-close, the buyer discovered that some fuel transactions were treated as “vendor handled it,” but the legal liability still sat with the operating entity. Result: amended filings and a tightened quarter-close process.

High-growth SaaS and benefits company: the company moved to a different health plan structure and did not realize it shifted PCORI filing responsibility. The tax was not huge, but the compliance miss created board-level concern because it was avoidable.

The takeaway is not that remittance taxes are always large. It is that they are process-driven, and weak process is what becomes expensive.

2026 trend: more complexity, more need for clean processes

Several trends are pushing remittance-tax compliance into the CFO’s “must systematize” category:

More bundled pricing and hybrid services in communications and transportation, increasing line-item classification risk.

More digital records (ERP, billing platforms, fuel systems), which makes reconciliation easier, but also makes inconsistencies more visible in audits.

Operational scaling (more locations, more SKUs, more vendors), which increases the chance that a taxable event happens without a tax team noticing.

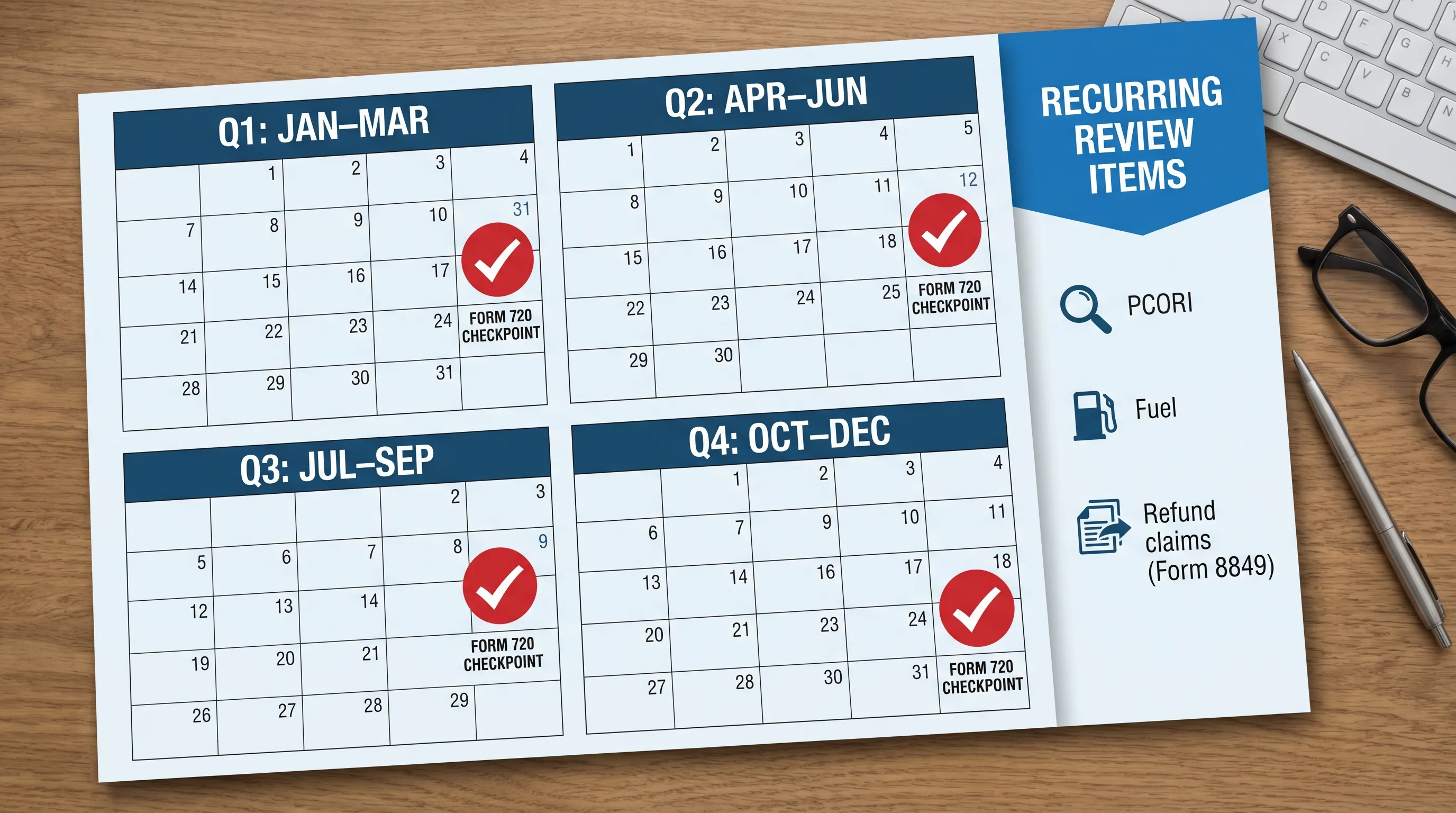

Practical workflow: a simple remittance-tax control stack

A lightweight but effective control stack usually includes:

A quarterly “taxable events” review with operations and billing

A reconciliation between GL accounts (tax payable, pass-through charges) and Form 720 categories

Document retention rules for exemptions and refunds (especially fuel)

A repeatable filing method that produces proof of submission and reduces manual errors

If you want to reduce admin time, form 720 online filing can be a strong fit, especially when your team wants an audit trail and less paper handling.

Filing option: file Form 720 online with eFileExcise720

If your remittance tax obligation is reported on Form 720, you can file Form 720 online through eFileExcise720, an IRS-authorized e-filing platform designed for Form 720 and related filings. The goal is to keep compliance straightforward: no software download, secure handling of data, and support when you have category questions.

Depending on your situation, you may also need to handle amendments (Form 720-X) or refund claims (Form 8849). If so, build a single workflow that keeps your reporting, corrections, and claims consistent from quarter to quarter.

Frequently Asked Questions

What is remittance tax USA and is it the same as sales tax?

Remittance tax USA is a broad concept, it means taxes a business must pay over to a taxing authority. Sales tax is one example at the state level, while many federal remittance-style obligations are excise taxes reported on IRS Form 720.

Who needs to remit federal excise taxes?

The party legally liable for the taxable event must remit. That can be a service provider, manufacturer, importer, fuel business, or an employer responsible for fees like PCORI, depending on the tax.

Where do I find form 720 filing instructions?

The IRS publishes official Instructions for Form 720, which explain categories, lines, schedules, and reporting rules.

Can I do Form 720 online filing instead of mailing paper forms?

Yes. Many businesses choose to e-file for speed, fewer manual steps, and electronic acknowledgments.

What is Form 8849 Schedule 1 used for?

Form 8849 Schedule 1 is commonly used for certain refund claims tied to nontaxable uses of fuels, when the claimant meets IRS requirements and has proper documentation.

Is PCORI filing part of remittance tax?

In practice, yes. The PCORI fee is reported and paid on Form 720, so it functions like a remittance obligation for the responsible plan sponsor.

Make remittance tax compliance a quarterly routine

If your business has any Form 720 exposure (fuel, communications, transportation, environmental categories, or PCORI), the best time to reduce risk is before quarter-end. You can create an account and file securely online with eFileExcise720 to streamline reporting, reduce paper processes, and get help when you need it.