What Is Form 8849 Claim for Refund of Excise Taxes? A Complete Guide

If you have ever looked at your federal excise tax activity and wondered, Did we overpay? you are not alone. In many industries, excise tax is embedded in fuel invoices, collected at the point of sale, or reported on Form 720, which makes overpayments easy to miss. That is where the Form 8849 claim for refund of excise taxes comes in: it is the IRS mechanism many taxpayers use to request a refund (or credit) when excise tax was paid but should not have been, or when a refundable credit applies.

This guide explains what IRS Form 8849 is, when it is the right tool and when it is not, and how to make your claim more defensible and faster to process.

What is Form 8849 Claim for Refund of Excise Taxes?

Form 8849 is an IRS tax form used to claim a refund of certain federal excise taxes, or to claim specific excise tax credits. Most claims relate to fuels (for example, nontaxable use of fuel, alternative fuel credits, or ultimate vendor claims), but the form also supports other excise refund categories depending on your facts and the applicable schedule.

In practical terms, Form 8849 is used when:

You paid excise tax as part of a transaction, but the tax should not have applied (or applied at a lower rate).

You qualify for a refundable excise credit and are requesting payment.

The IRS publishes official guidance in the Form 8849 instructions, including time limits, schedules, and recordkeeping expectations.

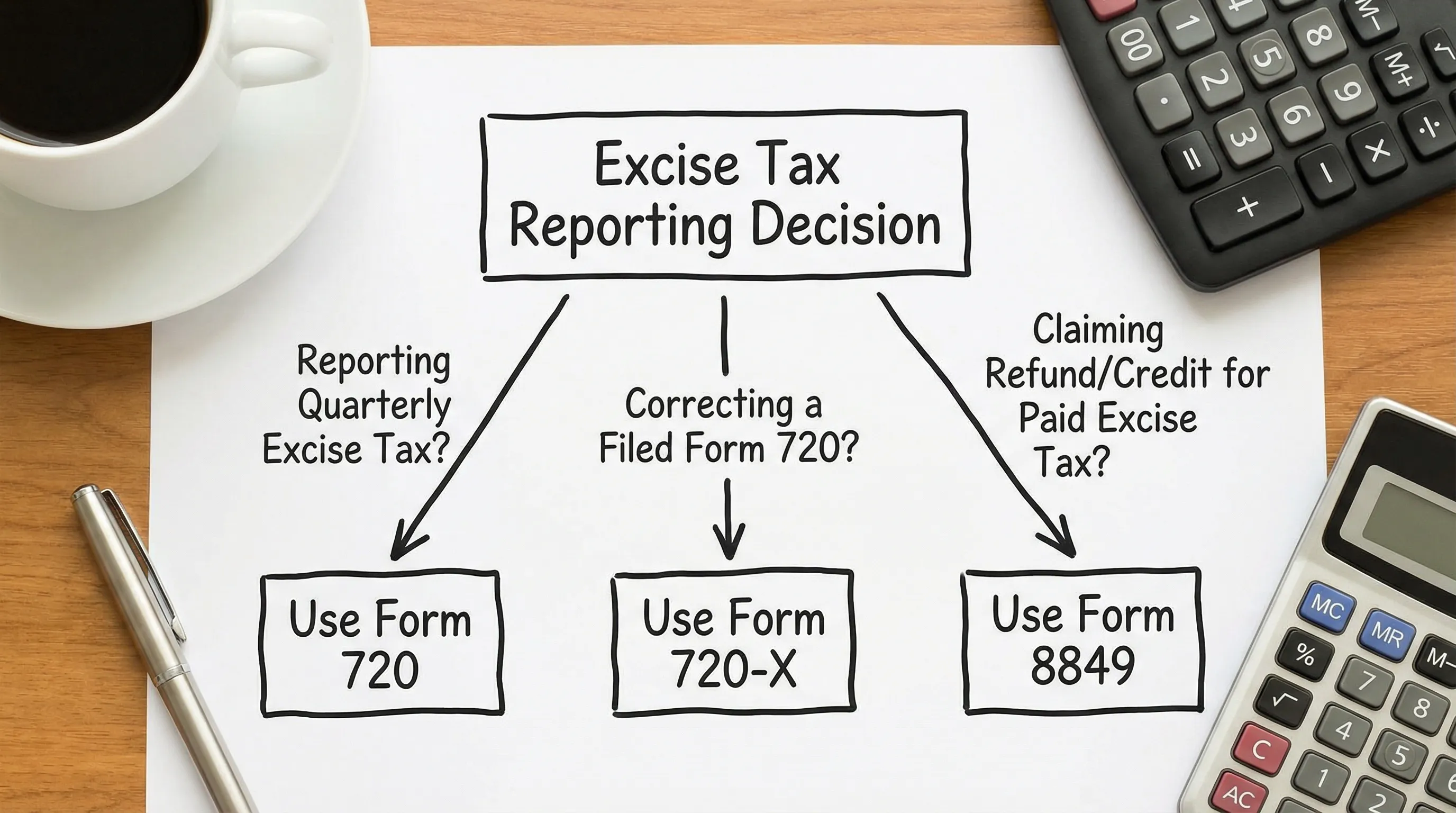

Form 8849 vs Form 720 vs Form 720-X

One of the biggest processing delays happens when filers pick the wrong form.

| Situation | Use This Form | Why It Matters |

|---|---|---|

| You need to report quarterly excise tax liability (and pay if due) | Form 720 | This is the core quarterly federal excise tax return. |

| You already filed Form 720 and need to correct tax reported (increase or decrease) | Form 720-X | Designed specifically to adjust a prior 720 filing. |

| You are claiming a refund/credit of certain excise taxes (often fuel-related) based on eligibility rules | Form 8849 | Used for refund claims that fit Form 8849 schedules and substantiation rules. |

Where the PCORI fee fits

Many people searching for pcori 720 form are really trying to fix an overpayment or correct a count. The PCORI Fee is generally reported and paid on Form 720. If you need to correct a PCORI amount after filing, the appropriate path is typically Form 720-X, not Form 8849.

What excise tax claims are commonly filed on Form 8849?

Form 8849 is structured around schedules. The exact schedule you use depends on the type of claim (for example, nontaxable fuel use vs ultimate vendor claims vs alternative fuel credits). The IRS details the current schedule set and eligibility rules in the instructions.

At a high level, organizations tend to use tax form 8849 in scenarios like:

Fuel used in a nontaxable way (for example, certain off-highway business use that meets IRS rules).

Ultimate vendor claims (when the vendor, not the end user, is eligible to claim a refund in defined cases).

Alternative fuel or mixture credits (where applicable and properly supported).

If you are unsure whether your situation belongs on Form 8849 or Form 720-X, it is worth validating early. Rework is costly because it can reset your internal approval cycle and delay cash recovery.

Deadlines and time value strategy: treat 8849 like a recurring recovery process

A refund claim is not just compliance, it is a cash cycle. Most excise refund opportunities become found money only if you create a repeatable process.

Two timing points matter:

- IRS time limits: Excise refund claims are subject to statutory time limits the IRS describes these in Form 8849 instructions. Missing the window can convert a valid claim into a permanent loss.

- Operational cadence: Many companies do not discover eligibility until year-end, which can compress timelines and increase error risk.

A practical strategy used by disciplined finance teams is a quarterly excise recovery review, similar to how they reconcile sales tax exemption certificates.

| Step in a Quarterly Recovery Review | What You Are Looking For | Documentation to Pre-Stage |

|---|---|---|

| Map transactions to excise categories | Which purchases/sales included embedded excise tax | Vendor invoices, product/fuel descriptions |

| Identify eligibility triggers | Nontaxable use, resale, qualified credits | Usage logs, customer exemption support (if applicable) |

| Validate claim ownership | End user vs vendor eligibility | Contracts, registration status, vendor attestations |

| Build an audit-ready file | Tie amounts back to source documents | Reconciliation worksheet + source PDFs |

Substantiation: the difference between a clean refund and a painful IRS notice

IRS processing is often straightforward when claims are well-supported. The friction usually comes from gaps between the claim amount and the underlying records.

Strong Form 8849 substantiation typically includes:

Clear linkage from the claim line to source invoices.

A reconciliation that shows how gallons, units, or taxable bases were calculated.

Proof that the claimant is the party entitled to the refund (a common issue in ultimate vendor scenarios).

Consistent recordkeeping across locations, vehicles, or business units.

From a lessons learned perspective, businesses that do this well treat excise substantiation like revenue accounting: one standardized method, one shared folder structure, and periodic internal checks.

Market insight: why Form 8849 scrutiny has increased for many filers

Even though Form 8849 is not new, the business environment around excise claims has changed:

More data trails exist (fleet cards, telematics, detailed invoices). That is good for substantiation, but it also means inconsistencies stand out.

E-filing has become the norm across tax administration, and the IRS continues to push digital workflows. The IRS Data Book shows electronic filing dominates many return types, and taxpayers increasingly expect faster confirmations and fewer manual errors.

Filing support: where eFileExcise720 can help

If you already file Form 720 including Form 720 PCORI reporting and you are extending your compliance to include refund claims, the operational win is having one place to manage the workflow.

eFileExcise720.com is an IRS-authorized platform for Form 720 e-filing and provides guided support for related excise workflows, including Form 8849 claims support, amendments via Form 720-X, and Form 8849-adjacent refund claim organization. If your goal is to file for IRS excise requirements with fewer surprises, a structured, dashboard-based process can reduce missed fields, mismatched quarters, and documentation gaps.

FAQs

What is a Form 8849 claim for refund of excise taxes used for?

Form 8849 is used to request a refund or credit for certain federal excise taxes already paid, commonly in fuel-related scenarios when the tax should not have applied or a refundable credit is allowed.

Is Form 8849 the same as Form 720?

No. Form 720 is the quarterly return used to report and pay excise taxes. Form 8849 is used to claim refunds or credits for eligible excise taxes.

If I overpaid the PCORI Fee, do I use Form 8849?

Usually, PCORI Fee corrections are handled by amending the original Form 720 using Form 720-X. PCORI is reported on Form 720 (the “pcori 720 form”), not typically refunded via Form 8849.

What documents should I keep for IRS Form 8849?

Keep invoices showing the excise tax paid, calculation worksheets, eligibility support (like usage logs), and proof that you are the proper party to claim the refund, as described in the Form 8849 instructions.