Form 720 for Fuel Distributors: Federal Excise Tax Filing Requirements Explained

Fuel distribution is a volume business. When margins are measured in pennies per gallon, a small classification error or missed deposit can turn into a material liability fast. That is why Form 720 for Fuel Distributors is not just a quarterly compliance task, it is a cash flow and risk management process.

In 2026, that pressure is rising. Renewable blends, more complex supply chains (terminal racks, exchanges, imports), and increasingly data-driven IRS matching mean fuel excise reporting needs the same discipline you apply to inventory and AR. This also ties directly into refund opportunities, where properly documenting credits through Schedule 6 Form 8849 can help recover overpaid fuel excise taxes and improve overall cash flow.

What Form 720 covers for fuel distributors and why it is different than income tax

IRS Form 720 is the Quarterly Federal Excise Tax Return. For fuel distributors, the return is typically driven by federal excise tax on taxable fuel transactions, reported quarterly, but often funded through more frequent deposits depending on your facts.

Key difference versus income taxation filing: excise tax is transaction-based and operational. It ties directly to physical movements (removals, sales, uses) and documentation (bills of lading, terminal reports, rack tickets), not just revenue recognition.

If you operate at the rack, hold positions in a terminal, blend, import, export, or sell fuel for taxable uses, you may have federal excise exposure that belongs on Form 720.

Common filing triggers in Fuel Excise Tax Filing

Fuel excise rules depend heavily on what you do in the supply chain. The same gallon can be taxable at one point and creditable later, depending on how it is removed, sold, and used.

Typical fuel-distribution activities that often drive Form 720 excise tax reporting include:

- Taxable removals of fuel from a terminal rack.

- Sales of taxable fuel for nonexempt uses.

- Blending activities (when blending creates a taxable event or changes product classification).

- Imports of taxable fuel.

- Sales that later become credits or refunds (for example, taxed fuel used in a nontaxable way, if you are the party eligible to claim).

Because responsibility can fall on different parties (terminal operator, position holder, blender, importer), one of the highest ROI exercises you can do is to write a one-page excise responsibility map for your business: who is liable, at which point, based on which document.

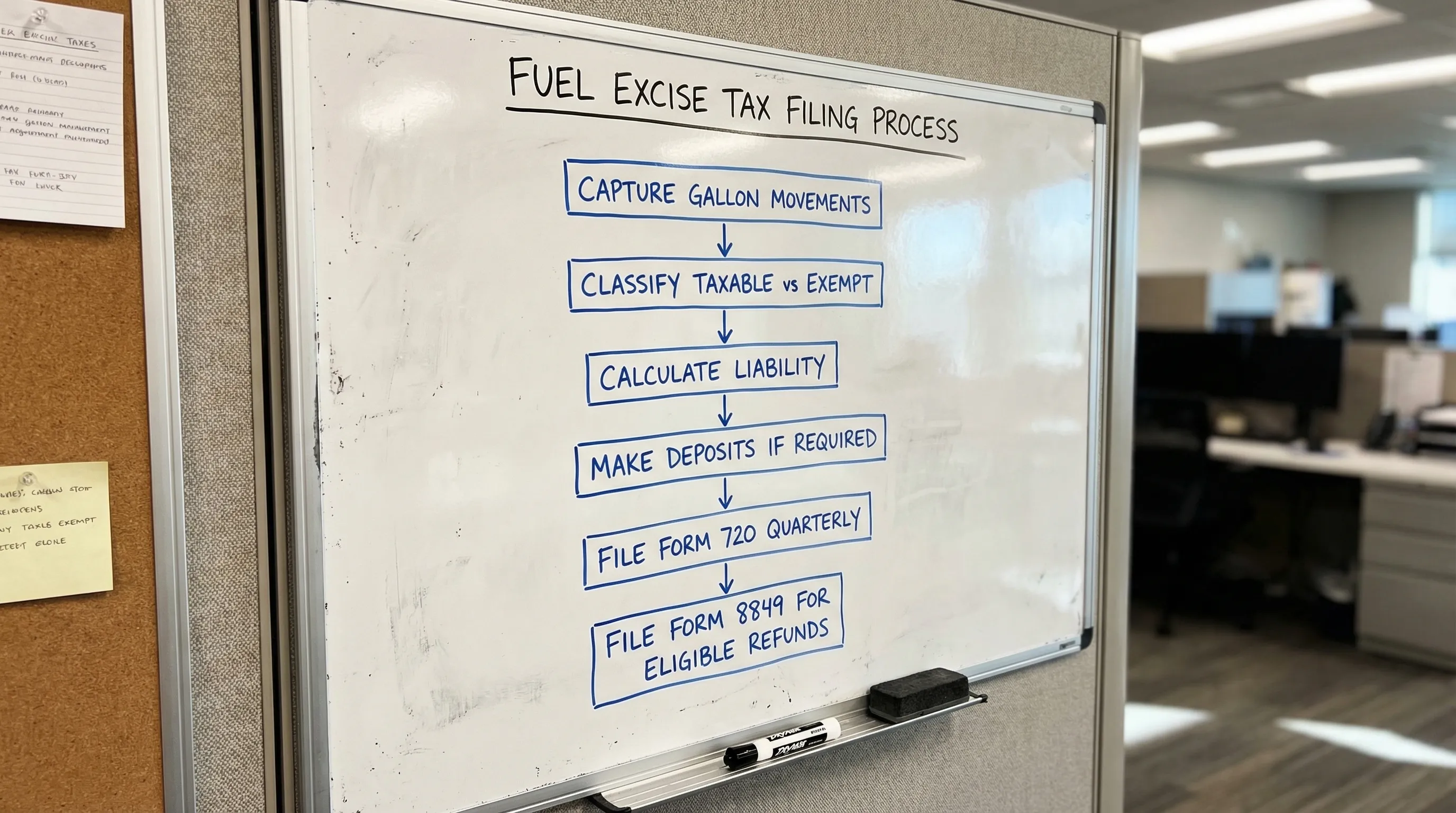

The forms fuel distributors actually use: Form 720, 8849 form, and amendments

Fuel distributors rarely live in a one-form world. A clean process usually involves three tools:

| Tool | What It Is Used For | Typical Fuel-Distributor Scenario |

|---|---|---|

| Form 720 | Quarterly reporting and payment of federal excise tax | Reporting liability for taxable fuel transactions during the quarter |

| Form 8849 | Claiming refunds of certain excise taxes | Claiming eligible refunds (for example, certain nontaxable uses) with required schedules and substantiation |

| Form 720-X | Correcting a previously filed Form 720 | Fixing misclassified gallons, wrong quarter, or other prior-period corrections |

The practical strategy is to decide upfront what you will handle as:

Credits on Form 720 (when eligible and supported), versus

Refund claims on Form 8849, versus

Corrections via Form 720-X.

That decision should be consistent, documented, and auditable. In diligence and IRS exams, inconsistency is often what creates follow-up questions.

How fast errors scale, a simple rate table you can sanity-check

Fuel excise tax is a per-gallon model. That means your exposure scales linearly with volume.

Here are two widely referenced federal excise rates you can use as a quick magnitude check (always confirm the exact taxability and current rates in IRS guidance for your product and use case):

| Fuel Type (Common Examples) | Federal Excise Tax Rate (Per Gallon) | Why It Matters Operationally |

|---|---|---|

| Gasoline (typical highway use) | $0.184 | A 100,000-gallon classification error can be $18,400 before penalties and interest |

| Diesel fuel (typical highway use) | $0.244 | The same 100,000 gallons can be $24,400, so controls on diesel movements are high impact |

These rates are discussed in federal excise resources such as IRS Publication 510. They are not a substitute for determining which line, use, and exception applies to your transactions, but they are helpful for setting materiality thresholds for reviews.

2026 trend watch: what is changing for fuel excise compliance

Fuel distribution keeps evolving, and compliance needs to keep up. Three trends are pushing more distributors to formalize their process:

More product complexity

As blending and alternative products expand, “what exactly is this gallon” becomes the core question. The best-run teams connect product codes and tax decisions at the SKU or bill-of-lading level, not in a spreadsheet after the fact.

Tighter documentation expectations

Claims and credits are only as good as your support. If you plan to use Form 8849 for refunds, build a standard packet now (transaction detail, counterparties, product description, taxable event proof, and use documentation). Treat it like a repeatable monthly close, not a scramble at quarter-end.

Investor scrutiny in acquisitions

Excise exposure is a classic diligence topic in downstream deals because it is high volume, rules-heavy, and sometimes under-controlled in fast-growth operations.

Real-world context: in large downstream transactions such as 7-Eleven’s acquisition of Speedway (announced 2020, closed 2021), investors know fuel operations are won or lost on tight controls and clean integration. Deal teams commonly evaluate whether excise processes scale with volume, whether deposit rules are consistently met, and whether documentation can support refund claims. The lesson for mid-market distributors is simple: a “good enough” process can become a purchase price adjustment when gallons multiply.

A practical control framework distributors can implement this quarter

If you want fewer surprises at filing time, focus on a few high-leverage controls:

- Monthly gallon reconciliation: tie terminal statements, rack tickets, and your invoicing system, then investigate variances.

- Taxability decision log: document why a category is taxable, exempt, or creditable, and keep it consistent quarter to quarter.

- Counterparty checks: confirm what your suppliers and customers are treating as the tax point, mismatches create double tax or missed tax.

- Claims readiness: for any expected tax form 8849 refund activity, standardize documentation before you file.

None of these require new software, but they do require ownership, a calendar, and a “single source of truth” for gallons.

How to handle edge cases (including PCORI 720 form overlap)

Most fuel distributors only think of Form 720 as a fuel return, but Form 720 is also used for other excise liabilities. A common example is the PCORI 720 form filing requirement for applicable self-insured health plans.

If your company has both fuel excise and PCORI responsibilities, treat them as two separate workstreams that share the same quarterly/annual Form 720 umbrella. The operational owners and documentation will differ, and merging them informally can lead to missed deadlines.

Form 720 online filing, and where eFileExcise720 fits

If you are still relying on manual workflows, form 720 online filing can reduce avoidable errors (like mismatched quarter selection, incomplete sections, or missing transmission proof) and speed up acknowledgments.

eFileExcise720 is an IRS-authorized e-filing platform built specifically to simplify Form 720 filing. It supports all Form 720 categories, offers secure data protection, includes free account creation with no software download, and provides personalized customer support. It also supports Form 720 amendments (720-X) and Form 8849 claims support, which is helpful when your fuel activity includes adjustments and refunds.

Frequently Asked Questions

Who must file Form 720 for fuel distribution activities?

Generally, businesses with taxable fuel transactions (such as certain removals, sales, or imports) may need to file Form 720. Because liability depends on your role in the supply chain, confirm your facts using IRS Form 720 instructions and Publication 510.

Is Form 720 filed monthly or quarterly for fuel distributors?

Form 720 is filed quarterly, but some taxpayers must make more frequent deposits depending on their excise tax liability and the rules that apply to their transactions.

When should a fuel distributor use Form 8849 instead of taking a credit on Form 720?

Use Form 8849 when you are claiming eligible refunds that are handled through the claims process and require supporting schedules. Whether to claim on Form 720 or Form 8849 depends on the specific credit/refund type and your documentation.

Can I fix a prior quarter fuel excise mistake after I filed Form 720?

Yes. Corrections are typically made using Form 720-X (amended return), rather than simply changing the next quarter numbers.

What documentation should I keep for Fuel Excise Tax Filing?

Keep transaction-level gallon detail, product descriptions, rack/terminal documentation, invoices, exemption certificates where applicable, and workpapers showing how you calculated liability, credits, or refunds.

Does Form 720 also cover PCORI fees?

Yes. PCORI fees are reported on Form 720 for applicable plan years. If you have both PCORI and fuel excise obligations, manage them as separate compliance tracks.

Get quarterly fuel excise filing done with less friction

Fuel excise compliance is manageable when your process is built around gallons, documentation, and repeatable checks, not last-minute quarter-end reconstruction. If you want an IRS-authorized way to complete Fuel Excise Tax Filing and Form 720 for Fuel Distributors with secure handling and dedicated support, you can file online through eFileExcise720.