Who Qualifies for the Fuel Tax Credit in the U.S? A Complete Guide

Fuel excise taxes are built into the price you pay at the pump. That is why many businesses do not realize they may be eligible to get some of that money back.

The key is simple. If you paid federal fuel tax but you used the fuel in a way the IRS treats as non-taxable, then a credit or refund may be available.

Fuel Tax Credit Eligibility Guide for U.S. Filers

What is the fuel tax credit and why does it exist?

Federal excise tax applies to many fuels sold for highway use. For example, the federal tax rate is 18.4 cents per gallon on gasoline and 24.4 cents per gallon on diesel fuel. These taxes help fund federal transportation programs.

But not every gallon is used on public highways. Fuel used in certain off-highway business activities or other approved uses may qualify for a fuel tax credit. In practice, this credit is a way to avoid paying highway tax on fuel that did not support highway use.

For definitions and category details, the most common starting point is IRS Publication 510, which covers excise taxes including fuel tax rules.

To answer who qualifies for the fuel tax credit, focus on three requirements:

- You paid federal excise tax on the fuel when you bought it

- You used the fuel in a qualified non-taxable way under IRS rules

- You can prove the gallons and the use with good records

In most cases, the claimant is the ultimate buyer of the fuel. That means the person or business that actually used the fuel for the qualified purpose.

Qualified use 1: Off-highway business use

Many fuel tax credits start here. If you use taxed fuel in equipment that does not drive on public roads, you may qualify.

Common examples include:

- Construction equipment such as loaders, bulldozers, and excavators

- Mining and quarry equipment

- Stationary generators or pumps used for business operations

- Forklifts and yard equipment used on private property

A simple way to understand this is: If the fuel is used to do work on private property and not to move a vehicle on public roads, it may qualify.

Qualified use 2: Farming use

Fuel used on a farm for farming purposes can qualify in many cases.

Examples include:

- Tractors and harvesters

- Irrigation pumps

- Farm machinery used off public roads

Farming claims can be valuable because farms often consume large volumes during planting and harvest seasons.

Qualified use 3: Certain government and nonprofit uses

Certain governmental entities can claim refunds in specific situations when they paid fuel tax but the use qualifies under the rules.

Nonprofits sometimes assume they automatically qualify. That is not always true. Eligibility depends on the exact use category in IRS guidance.

Qualified use 4: Other specific non-taxable uses

Depending on your facts, additional categories may apply such as specific uses of aviation fuel, marine use, or certain commercial use cases defined in the instructions.

Because the rules vary by fuel type and use category, it is smart to confirm your situation using Form 8849 instructions or a tax professional.

Fuel types and a practical reality check

A common mistake is to assume any off-road fuel qualifies.

The credit usually depends on whether federal excise tax was actually paid on the gallons you are claiming.

For example, dyed diesel is generally sold as a non-taxed fuel for off-highway use. If no federal excise tax was paid, there is usually no credit to claim for those gallons.

Quick math you can use to estimate potential value

This table gives a simple way to estimate your potential benefit using the common federal rates for gasoline and diesel.

| Fuel type | Federal excise tax rate | Example gallons used in qualified use | Estimated potential credit |

|---|---|---|---|

| Gasoline | $0.184 per gallon | 10,000 gallons | $1,840 |

| Diesel | $0.244 per gallon | 20,000 gallons | $4,880 |

These are not promises of refunds. They are quick planning numbers that help you decide if tracking and filing is worth the effort.

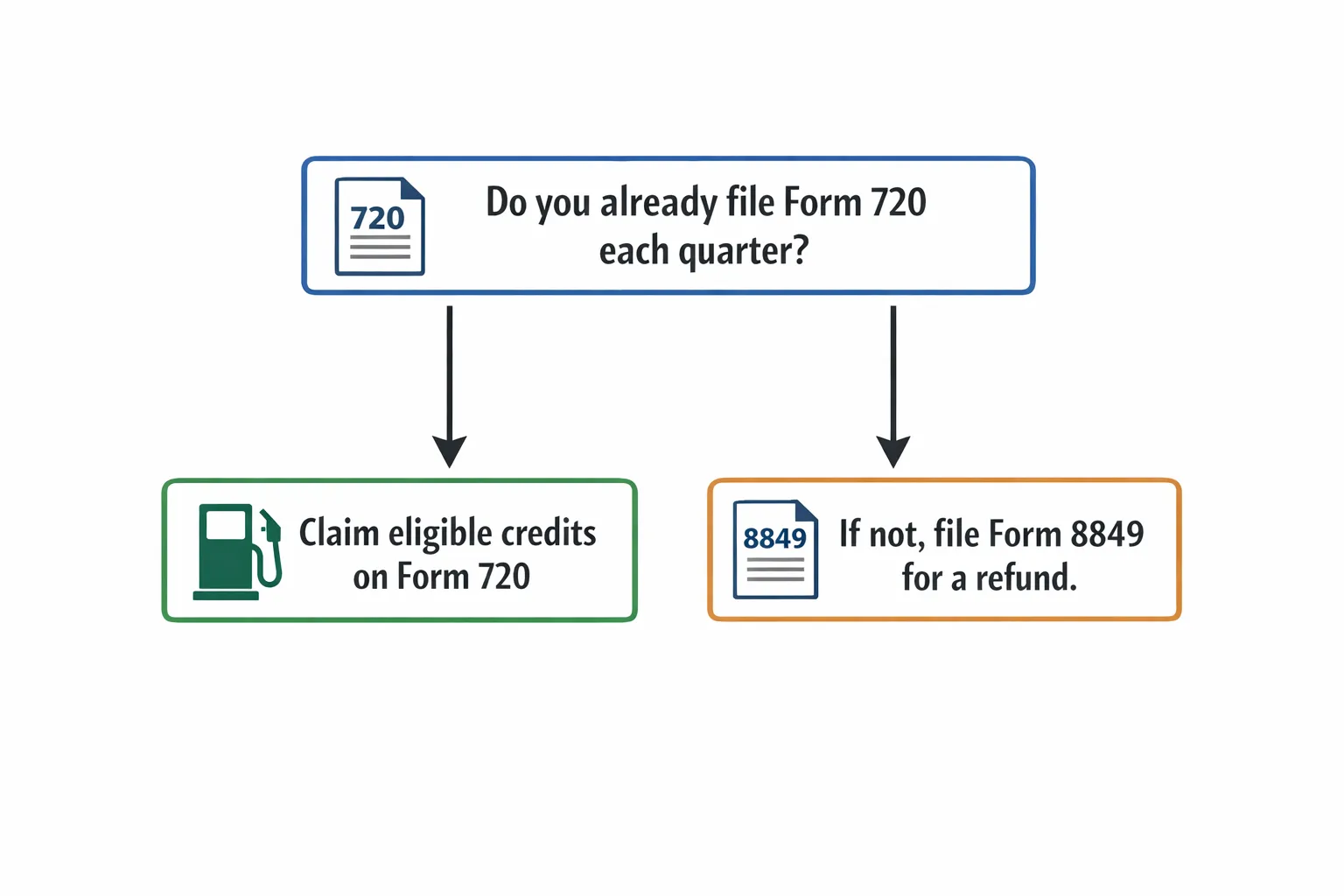

Which form should you use: Form 720 vs Form 8849?

Many businesses get stuck here. The best form depends on whether you already file Form 720 and on what type of claim you are making.

Option A: Claim on Form 720 when you already file quarterly

If your business files IRS Form 720 for other excise taxes, you may be able to claim certain fuel credits on the return for that quarter (often through Schedule C depending on the category).

This can reduce what you owe for the quarter.

Option B: File Form 8849 to claim a refund

If you do not file Form 720 or if your claim belongs in a refund process, you may use Form 8849 to request a refund of excise taxes.

This is common for off-highway users who do not otherwise have quarterly excise tax liability.

Where does Form 4136 fit?

Some filers claim fuel credits on their income tax return using Form 4136. Since this guide is focused on excise filing workflows, always confirm which path applies to your situation in the IRS instructions or with your tax preparer.

Here is a simple decision table you can use for planning.

| Your situation | Common filing path | Why it is used |

|---|---|---|

| You already file Form 720 for excise taxes | Claim eligible credits on Form 720 when allowed | You are already reporting quarterly excise activity |

| You do not file Form 720 and want a fuel tax refund | File Form 8849 | You are requesting a refund for eligible non-taxable use |

| You want to claim with your income tax filing | Consider Form 4136 | Often used with annual income tax returns |

Strategic advice: what strong claimants do differently

Fuel tax credit dollars are real, but the IRS expects strong documentation. The best filers treat this like a controls process, not a once-a-year guess.

Trend: better tracking is turning credits into predictable cash flow

More businesses now use fuel cards, telematics, and equipment hour meters to separate highway use from off-highway use. That separation makes the credit easier to defend.

A practical lesson learned from fleet-style businesses is that the credit becomes much more reliable when:

- Off-highway equipment has its own fueling process

- Drivers and operators log gallons by unit or job site

- Reports match invoices and payment records

Example 1: Construction company that stopped leaving money on the table

A mid-size contractor buys diesel for highway trucks and job-site equipment. In prior years, they could not support off-highway gallons, so they skipped the credit.

After they added a simple rule (job-site tanks for equipment only and a monthly gallons report), they could estimate qualified gallons with much higher confidence. If the company can document 20,000 qualified gallons, the planning value at 24.4 cents is about $4,880.

The takeaway is not the number. The takeaway is that the credit often depends more on tracking discipline than on tax complexity.

Example 2: Farm operation that aligned purchases with usage logs

A farm using gasoline in several pieces of equipment kept receipts but not usage logs. When they matched each invoice to equipment hour logs, they reduced uncertainty and made the claim easier to review.

If the farm documents 10,000 qualified gallons of gasoline, the planning value at 18.4 cents is about $1,840.

Common mistakes that delay refunds or reduce credits

Most fuel tax problems are paperwork problems.

- Claiming gallons that were not taxed (common with dyed diesel)

- Mixing on-road and off-road use in one total without support

- Missing invoices or using vendor summaries that do not show gallons

- Using estimates with no method or written policy

- Filing under the wrong claim category or schedule

- Forgetting that some claims have timing limits and documentation rules

If you want the exact rules for your claim type, use the official instructions for Form 720 and Form 8849.

How this relates to other Form 720 filings like the PCORI Fee

Many companies come to Form 720 for fuel tax. Others come because they owe a different excise tax such as the PCORI Fee.

The important comparison is this: PCORI Fee is a healthcare-related fee reported on Form 720 for many plan sponsors. Fuel tax credits and refunds are based on how fuel was used and how the fuel tax was paid.

If your business touches both areas, a single quarterly excise workflow can reduce missed deadlines and reduce rework.

For a broader view of quarterly excise reporting, you can also read this guide on federal excise tax guide .

Filing online with eFileExcise720

If you want a simpler way to file Form 720 or prepare fuel-related refund claims, eFileExcise720 is an IRS-authorized e-filing portal built for excise tax compliance. You can create an account for free and file online without installing software.

If you are comparing providers, focus on three practical points:

- IRS authorization and data security

- Support when you are unsure about a category or a correction

- Clear workflow for Form 720 amendments (720-X) and Form 8849 claims

To start filing, visit eFileExcise720. For pricing or help choosing the right form, use pricing or contact us.

Quick answers to common fuel tax credit questions

Who qualifies for the fuel tax credit if they run heavy equipment?

You may qualify if you paid federal fuel tax and used the fuel in equipment for off-highway business use with clear records that support gallons and usage.

Can I claim a credit if I used dyed diesel?

Usually no, because dyed diesel is generally sold without federal excise tax for off-highway use. No tax paid usually means no credit.

Do I need Form 720 or Form 8849 for a fuel tax refund?

Many businesses use Form 8849 for refunds. If you already file Form 720, you may be able to claim certain credits on Form 720 for that quarter. Always confirm the correct method for your claim type.

What records should I keep for a fuel tax claim?

Keep fuel invoices, proof of payment, usage logs by equipment or vehicle, dates, locations, and a method that separates highway from off-highway use.

Can the fuel tax credit apply to farming?

Yes, in many cases fuel used on a farm for farming purposes can qualify when tax was paid and the use meets IRS rules.

Does eFileExcise720 support Form 8849 and Form 720?

The platform supports Form 720 filing and also supports Form 8849 claims, which helps businesses handle both quarterly reporting and refund requests in one place.

Our services are also available for 720 filing California, 720 filing Florida, 720 filing Illinois, and form 720 filing Texas.