Form 720 for Health Plan Sponsors: A Complete Guide to PCORI Filing

Health plan sponsors often treat the Patient-Centered Outcomes Research Institute (PCORI) fee as a once-a-year compliance chore. In practice, it’s a repeatable workflow that involves benefits administration, payroll, finance, and occasionally M&A integration. For 2026, the sponsors that file smoothly are the ones that treat PCORI like a mini tax close, with clear ownership, reliable covered-life data, and a documented method that can stand up to questions later.

This guide explains Form 720 for Health Plan Sponsors (PCORI), including who pays PCORI fees, how to calculate it, and how to handle form 720 online filing with fewer surprises.

What the PCORI fee is and why sponsors should care

The PCORI fee funds research intended to improve health outcomes and the quality of healthcare decision-making. It is reported annually on IRS Form 720 (Quarterly Federal Excise Tax Return), even though the PCORI fee itself is not filed quarterly.

From a risk standpoint, PCORI is usually low-dollar per covered life, but high-frequency operationally. One missed filing can trigger avoidable penalties and rework, especially if the sponsor is managing multiple plan options, multiple EINs, or has undergone acquisitions.

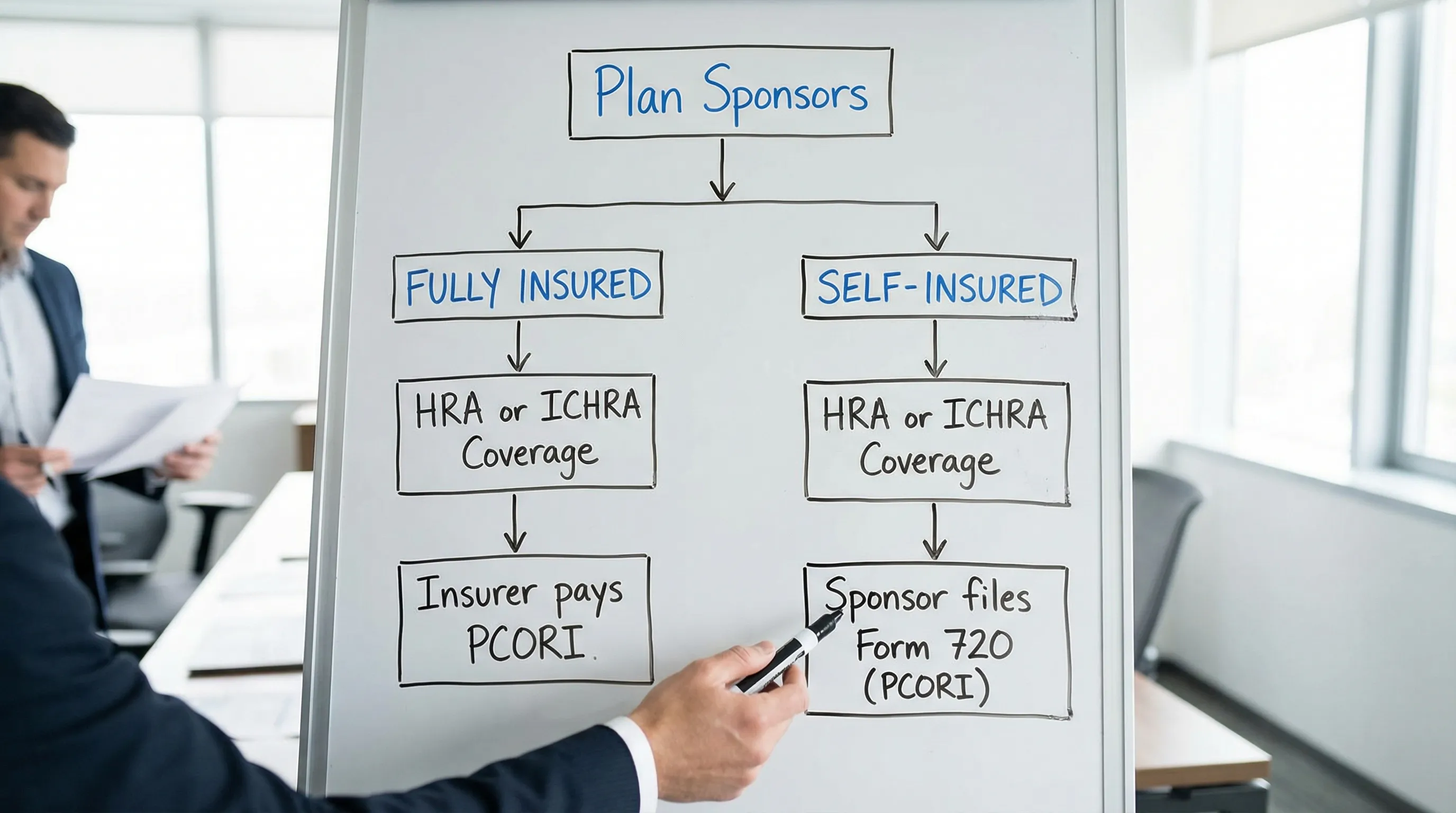

Who pays PCORI fees and the rules sponsors trip over

A key question is who pays PCORI fees. The answer depends on how the coverage is funded.

- Fully insured health plans: the insurer generally pays the PCORI fee.

- Self-insured health plans: the plan sponsor generally pays the PCORI fee.

Common edge cases where sponsors should slow down and confirm responsibility:

- Level-funded arrangements: these often look like fully insured plans operationally, but the sponsor may still be treated as self-insured for PCORI purposes depending on structure.

- HRAs and ICHRAs: many arrangements are treated as self-insured, which can create PCORI filing obligations even when the medical plan itself is fully insured.

- Multiple plans under one sponsor: you may owe PCORI for more than one arrangement, and each may use different covered-life data sources.

The IRS maintains PCORI background, filing mechanics, and rate updates on its official PCORI resource page: PCORI fee information.

The deadline: where PCORI is reported on Form 720

PCORI is filed on Form 720 using the second quarter Form 720 even if you have no other excise taxes. The due date is July 31 following the end of the plan year.

Example: If your plan year ends December 31, 2025, your PCORI filing is due July 31, 2026.

This is where many teams slip: they treat PCORI like a benefits renewal task, but it is actually tied to the plan year end, then reported on a tax form with a fixed July deadline.

Choosing a covered-lives counting method (strategic tradeoffs)

Most sponsor pain comes from the covered-lives calculation, not the rate. The best method is the one you can execute consistently and document.

| Counting method | What it uses | Strengths | Watch-outs |

|---|---|---|---|

| Actual count method | Day-by-day covered lives | High precision | Operationally heavy, requires clean eligibility feeds |

| Snapshot method | Covered lives on selected dates (plus permitted variants) | Efficient and defensible when documented | Must follow consistent snapshot date rules |

| Form 5500 method (when eligible) | Participant counts from Form 5500 | Low lift if your Form 5500 data is reliable | Only available for certain plan types and timing, confirm eligibility |

For detailed mechanics, always align with the IRS’s current form 720 filing instructions and PCORI guidance (start from Form 720 information on IRS.gov).

Market trends that make PCORI harder in 2026

PCORI itself has not become more complex, but sponsor environments have.

Trend 1: More self-funding, more sponsor responsibility

Self-funded coverage remains prevalent among larger employers, which increases the number of plan sponsors directly responsible for PCORI operations. The Kaiser Family Foundation (KFF) reports that a majority of covered workers at large firms are in self-funded plans. When sponsors move from fully insured to self-funded or level-funded, PCORI becomes their responsibility, often before the team has built a repeatable process.

Trend 2: M&A activity and portfolio complexity (a common investor-driven challenge)

A frequent real-world pattern in private equity-backed rollups and other acquisition-heavy employers is benefits fragmentation: multiple EINs, multiple TPAs, and multiple plan years running in parallel. The PCORI fee is small, but the coordination cost is not.

Lesson learned from these scenarios: centralize the PCORI workpaper (rate period, counting method, data source, assumptions, reviewer sign-off) and require each acquired entity to deliver covered-life inputs on a standard schedule.

Trend 3: Compliance teams are automating evidence collection

More sponsors are treating benefits compliance like other regulated workflows: standardized controls, audit trails, and task assignment. Some teams complement their filing process with compliance automation tools such as AI for compliance teams to streamline policy evidence, remediation tracking, and workflow ownership across departments.

A practical playbook for PCORI filing (built for repeatability)

If you want fewer last-minute scrambles, run PCORI like a small annual project.

1) Build a one-page PCORI control sheet

Include:

Which plans create PCORI liability (medical, HRA, ICHRA, other self-insured arrangements)

Plan year end date for each

Counting method selected and why

Source system for covered lives (TPA eligibility file, benefits admin, Form 5500)

Internal reviewer (finance or tax owner)

2) Pre-close your covered lives before July

Aim to finalize counts 30 to 45 days before July 31. That buffer is where you resolve mismatched eligibility files, retro terminations, or mid-year plan migrations.

3) Decide how you will file: paper vs pcori online

Sponsors increasingly prefer pcori online workflows because they shorten cycle time and reduce mailing risk. If you want form 720 online filing, an IRS-authorized e-file provider can guide you through the return and help you keep a clear submission record.

With eFileExcise720, sponsors can file Form 720 online through an IRS-authorized portal, without installing software, and with customer support available when questions come up during submission.

FAQ

Who pays PCORI fees for a fully insured plan?

Typically the insurer pays for fully insured plans, not the employer, although sponsors should confirm for any special arrangements.

Who pays PCORI fees for a self-insured plan?

Typically the plan sponsor pays the PCORI fee and reports it on Form 720.

When is PCORI due on Form 720?

PCORI is generally filed using the second quarter Form 720 and is due July 31 following the end of the plan year.

Can I do PCORI filing online?

Yes. Many sponsors choose electronic filing options pcori online to reduce mailing delays and get clearer proof of submission.

What records should we keep for PCORI filing?

Keep your covered-lives calculation support, method selection rationale, rate used, plan year dates, and proof of filing/payment in a central workpaper.